As we enter a new year, it’s time for our annual ritual of synthesizing the lessons from the past twelve months and formulating the outlook for the next twelve. Notably, when kicking off this thought exercise, we realized that several of the topics look similar to last year.

Though there are lots of developments and new insights, the topical containers that house those insights are beginning to coalesce into standard buckets. We’re talking mobile AR engagement & monetization; AR cloud development; enterprise AR and the gradual march of VR.

This standardization is good news in that it signals spatial computing’s exciting – yet insecure – early days have transitioned to an adolescent period of its lifecycle. We have a firmer grasp on what’s working….versus 2017’s wild speculation on the technology’s world-shifting impendence.

So where is spatial computing now, and where is it headed? What’s the trajectory of each of the above subsegments? This was the topic of the latest ARtillery report, Spatial Computing: 2020 Lessons; 2021 Outlook. It looks back and looks forward, including concrete predictions.

Prediction 5: VR’s Slow & Steady Rise

After examining enterprise AR in our fourth prediction last week, our fifth and final prediction moves on to VR. The short version of VR’s state of the union is that it represents a promising technology in gaming and entertainment, but its traction continues to be slow and steady.

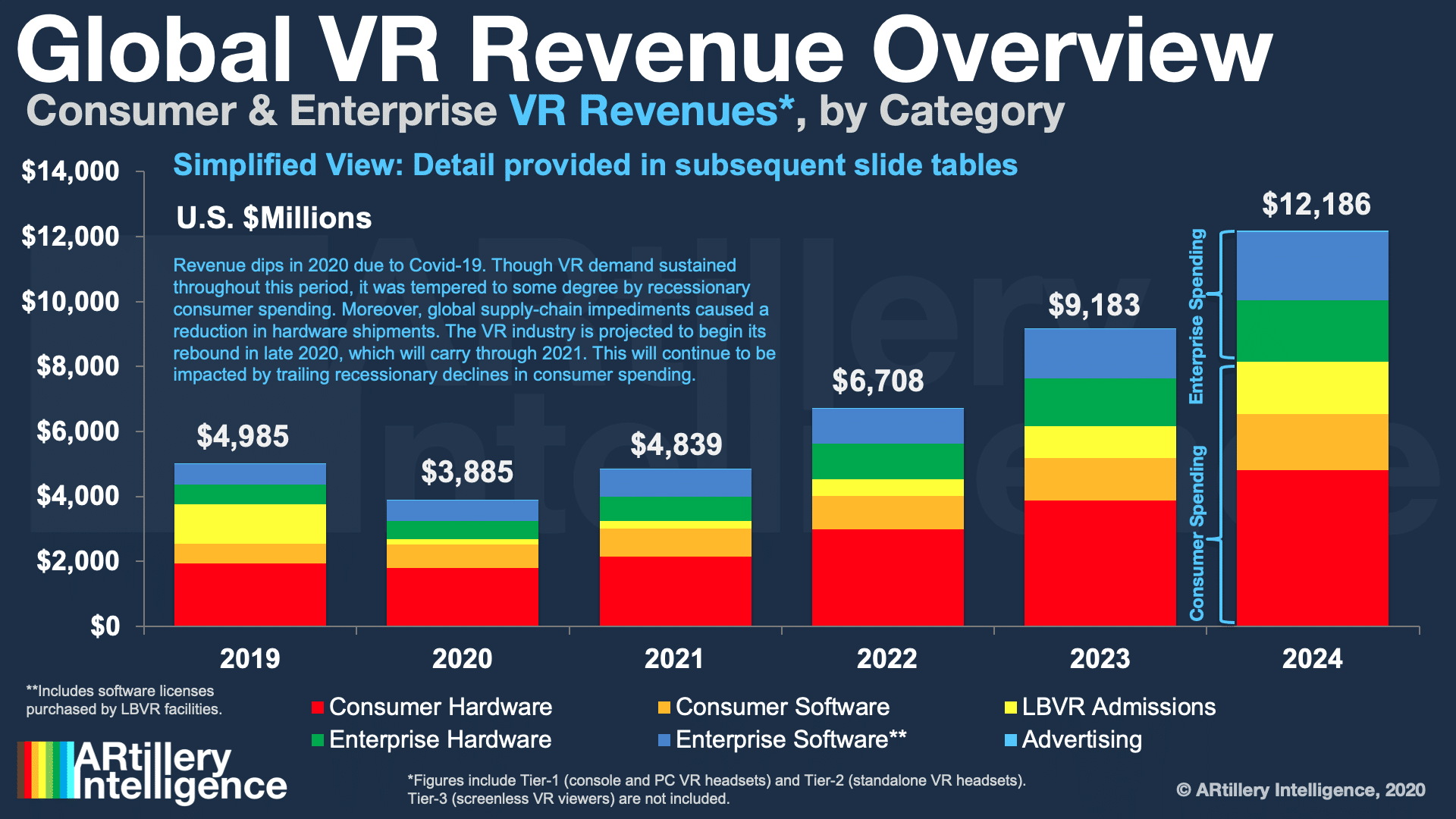

As recently estimated in ARtillery’s global VR forecast, sector revenue will grow from $4.98 billion in 2019 to $12.2 billion in 2024, a 19.6 percent compound annual growth rate (CAGR). This consists of consumer ($2.67 billion in 2020) and enterprise spending ($1.21 billion in 2020).

Consumer spending is driven by gaming’s lead as a VR use case. VR has valuable but relatively-narrow use in the enterprise due to its degree of sensory immersion that compromises safety, social presence, and ergonomics. But it is showing promise as a training tool.

Like many sectors, VR has been impacted by the ongoing Covid-19 global pandemic. Though demand has remained strong during global lockdowns (VR is aligned with Covid-era demand signals such as gaming), the industry has suffered from supply-chain impediments.

A Quest for Market Share

One key factor counteracting those declines is Facebook’s multi-billion-dollar investments to seed content, user demand, and compelling hardware. These investments come at a sizeable short-term cost for Facebook, but they advance the company’s long-term VR ambitions.

Facebook’s VR strategy is best embodied in its latest hardware: Oculus Quest 2. By all measures, the device is a hit. After pre-launch rumors of a cheaper ‘lite” Quest or a more-loaded “Pro” Quest….we ended up getting the best of both: upgraded and cheaper hardware.

One success metric is pro reviews, which are unanimous in their praise of the device. Not to take away from UX execution, one factor is Facebook’s aggressive pricing. Its long-term VR strategy lets it sacrifice near-term margins to build a network effect and win early market share.

This loss-leader pricing gives us a device that’s much cheaper than it should be. That’s great for consumers but the dark side of that equation is a device that’s very hard to compete against — especially for margin-dependent hardware players in Oculus’ competitive field.

Clues Emerge

But professional reviews and analyst speculation admittedly only go so far. The true test will be how the market receives Quest 2. The VR industry has been waiting for its hero device to get over the mainstream adoption hump — wheels that were greased to some degree by Quest 1.

We don’t know enough about Quest 2 sales yet but a few positive signals are emerging. That includes Facebook’s Q3 earnings call in which Mark Zuckerberg reported a 5x delta in pre-orders versus Quest 1. This comes after our September estimate of one-million Quest sales.

Looking forward, ARtillery Intelligence’s Global VR forecast projects Quest’s 2020 sales (including Quest 1 and 2) to be 770,000 units, growing to 1.42 million in 2021. Quest’s cumulative lifetime sales meanwhile reached an estimated 1.2 billion at the end of 2020.

These figures are based on Facebook disclosures, software/game sales, device availability, and a sizeable holiday marketing push. Given Quest 2’s potential to mainstream AR with compelling hardware and a giftable price point, Q4 sales could be its “moment of truth.”

Underserved Demand

Another signal that helps us extrapolate Quest 2’s sales volume is less about demand and more about supply. Facebook got a better sense of market demand with Quest 1, whose perpetual sold-out status throughout 2020 indicated underestimated and underserved demand.

In fairness, part of that undersupply was due to unexpected and Covid-inflicted supply-chain impediments. These exacerbated pre-Covid stock levels which were low or empty throughout most of the holiday 2019 timeframe (partially impacted by China’s early COVID onset).

Regardless of the reason, Oculus gained demand insights, which now inform Quest 2’s supply-chain strategy. It has scaled up to meet greater demand, so Quest 2’s penetration — big or small — at least won’t be supply-constrained. And it’s already working for the most part.

“We really couldn’t be happier,” Facebook Reality Labs’ Chris Pruett told Protocol in the only level of detail that he’s understandably allowed to say publicly. “The device is selling quite well…faster than Quest did…and maybe a little bit beyond what we expected.”

Boiling it Down

To synthesize all of the above into a concrete set of potential market outcomes, here’s what we think will happen in 2021:

— The VR world has come to terms with the fact that its revolutionary status trumpeted in the circa-2016 hype cycle was misguided.

— VR could transform several areas of media, entertainment, and enterprise productivity, but in narrower ways. And the timeline will be much longer.

— That said, 2020 was a positive year for VR (even with a global pandemic) and 2021 will accelerate the sector even more.

— This is mostly due to Oculus Quest 2, which continues to push the boundaries of consumer VR hardware, while having a compelling price to feature ratio (stemming from Facebook’s long-term investment and loss-leader pricing).

— We estimate 770,000 Quest 1 and 2 unit-sales in 2020 and 1.42 million Quest 2 unit-sales in 2021.

— Going forward, VR is positioned well due to its alignment with remote work and home entertainment.

— Though the world will start to bounce back from a pandemic in 2021, the post-Covid environment will maintain some new models discovered in 2020, including hybrid-levels of remote work, home entertainment, and other dynamics that align with VR adoption.

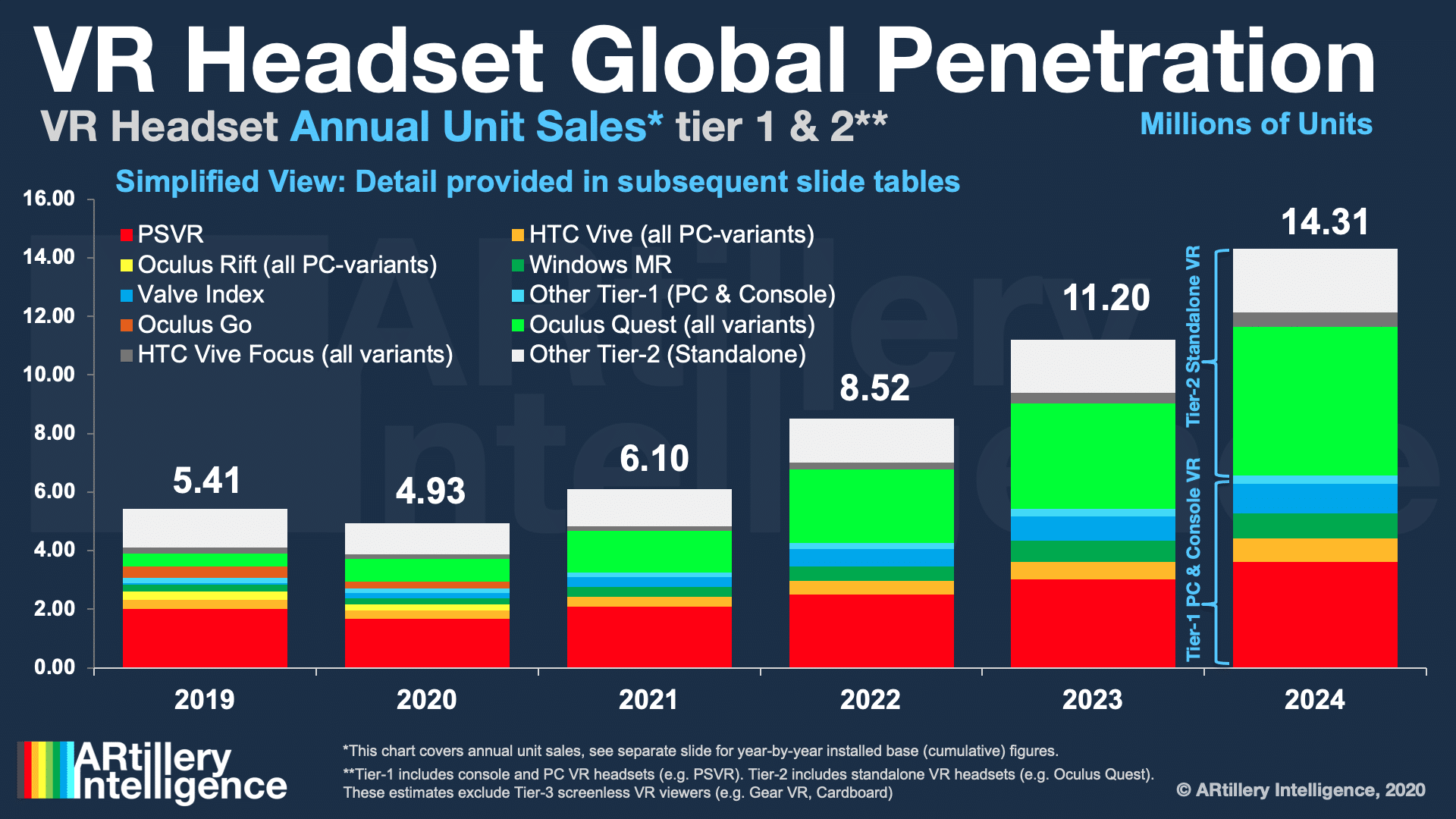

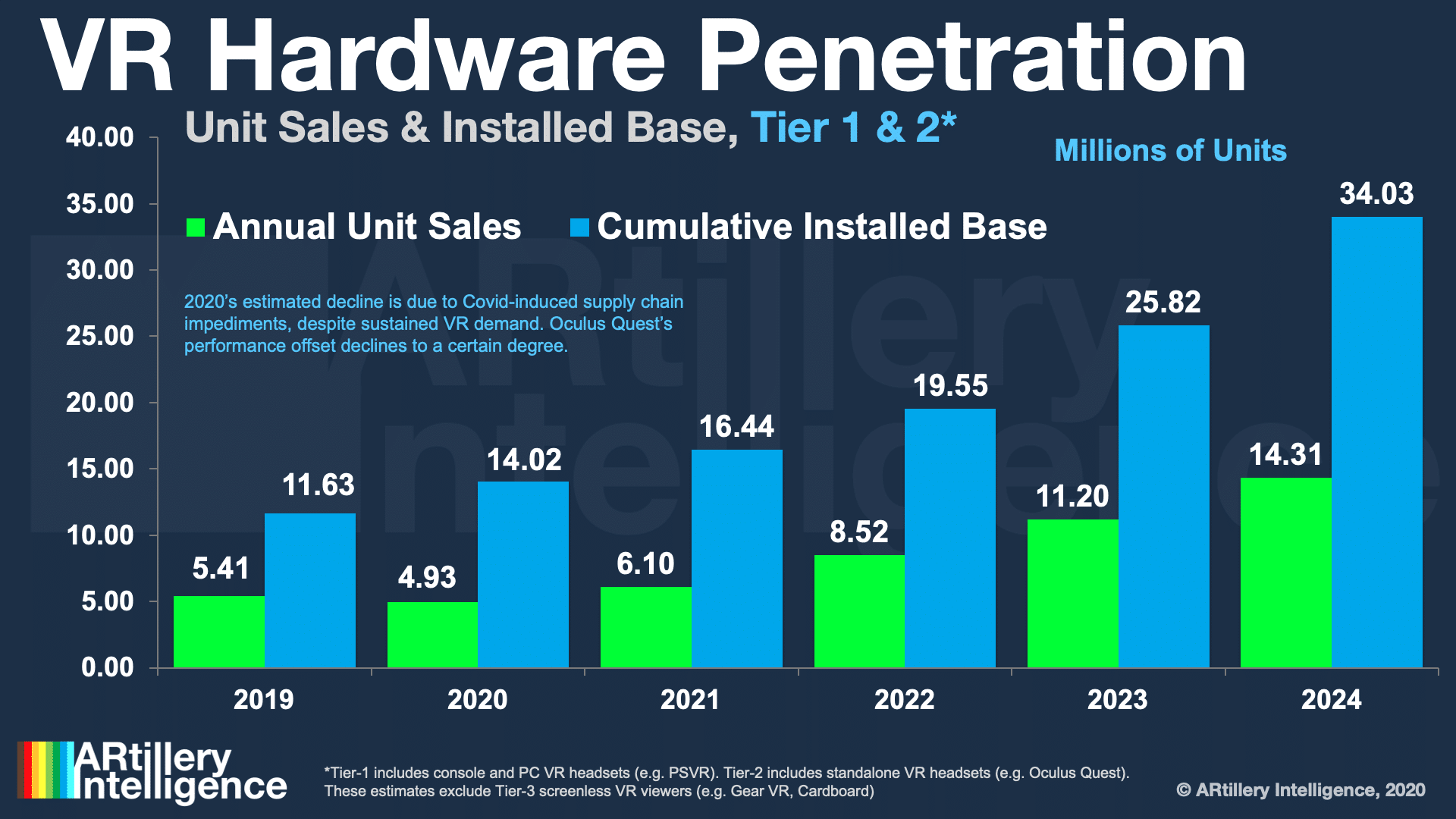

— We project tier 1 & 2 VR sales to reach 6.1 million units in 2021, while its cumulative in-market installed base grows to 16.4 million (see chart above).

— Tier 1 includes PC and console VR, while tier 2 includes standalone VR. Mobile VR screenless viewers (tier 3) such as Gear VR are not counted in the above figures.

See more in the full report and in the video below.