Wearables continue to be one of the fastest-growing product categories in consumer tech. This is notable given that all-things hardware are constrained during Covid-era lockdowns. Those headwinds result from supply-chain impediments and consumer-spending slowdowns.

This is indirectly but importantly relevant to AR. As we continue to examine, wearables are AR’s forbear, in that they will condition consumers to wear sensors on their bodies. That could eventually ease the cultural and stylistic acclimation to AR glasses, which will be an uphill battle.

Meanwhile, wearables are further propelled by tech-giant motivations. That’s especially true for Apple, which continues to double down on Watch and AirPods. It sees wearables both offsetting near-term iPhone revenue deceleration; and future-proofing its hardware-heavy profit machine.

As we’ve examined, Watch and Airpods could eventually converge with glasses in a holistic suite that augments reality from several angles. This could replace (or augment) the current suite of iThings, which notably fits the profile for Apple’s ARPU-driving multi-device ecosystem approach.

Trending Up in a Downturn

All of this was pushed forward in 2020 when several signs pointed to wearables growth. One such sign was IDC’s recent estimate that wearables will grow 15 percent in unit shipments in 2020. Growth in the category certainly slowed due to Covid-19, but was positive nonetheless.

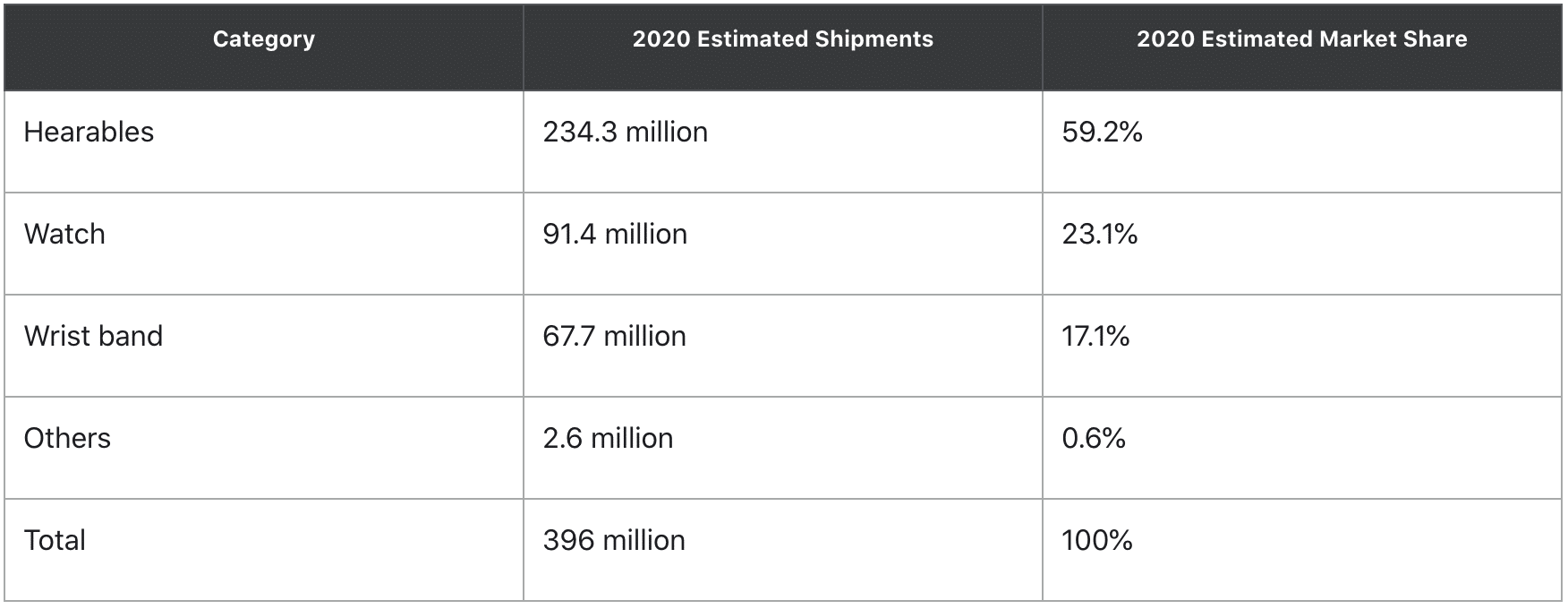

Breaking that down a bit, IDC estimates that global wearables unit sales grew from 346 million units in 2019 to 396 million units in 2020. This growth accelerated in Q4, due not only to holiday spending but new hardware including Apple Watch Series 6, Fitbit Sense and Airpods Pro.

Speaking of Airpods, hearables lead the wearables category with 59 percent market share. This is up from about 50 percent in 2019. IDC meanwhile projects 14.1 percent compound annual growth (CAGR) for hearables through 2024, and a 14.3 percent CAGR for smartwatches.

Another key trend driving wireless growth is software. Just as iPhone sales inflected when the app store was introduced a year after its launch, wearables utility and appeal are unlocked with more apps and experiences, including health trackers, geospatial awareness, and (eventually) AR.

Revenue Reconciliation

One question arises from all of the above: who’s leading? Though Google/Fitbit and Amazon are making headway, Apple continues to hold the largest market share with an estimated 66 million AirPods sold in 2020 (ARtillery Intelligence) and 80 million Apple watches (Above Avalon).

That brings us back to Apple and the earlier claim that it’s doubling down on wearables in the ongoing feedback loop that flows from the category’s success. Among other things, wearables are offsetting the continued revenue deceleration in Cupertino’s prized pig, the iPhone.

One example to quantify that comes from Apple’s 2020 fiscal Q2 earnings. It reported “wearables, home and accessories” revenue growing 24 percent ($1.2 billion), while iPhone sales fell 6.7 percent ($2.1 billion). The former doesn’t fully redeem the latter, but the offset is valued.

As noted, this revenue reconciliation is just one task that wearables have at Apple. The other is to buttress the iPhone succession plan, where Apple has a lot riding. There won’t be a single iPhone replacement, but an iPhone-dependent wearables suite — including glasses — is likely.