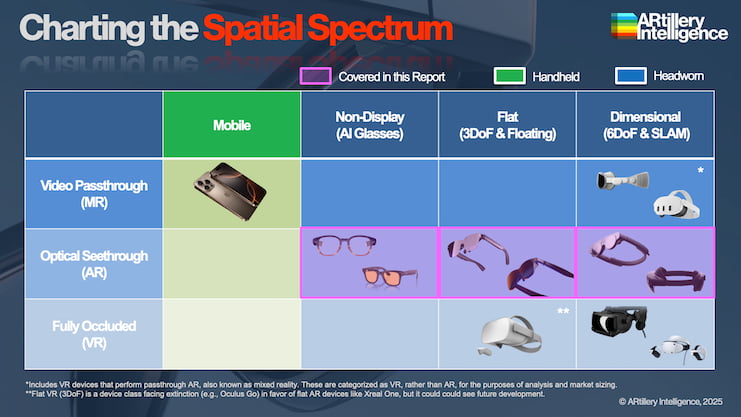

Like many analyst firms, market sizing is one of the ongoing practices of AR Insider’s research arm, ARtillery Intelligence. A few times per year, it goes into isolation and buries itself deep in financial modeling. One such exercise zeroes in on headworn AR revenues.

This is one of the main subdivisions of spatial computing – others include mobile AR and VR. They’re all related and share technological underpinnings, but are driven by separate market forces such as their respective hardware bases (see methodology and inclusions).

So what did the headworn AR forecast uncover? At a high level, global headworn AR revenue is projected to grow from $2.61 billion in 2024 to $14.02 billion in 2029, a 39.96 percent CAGR. This sum consists of consumer and enterprise spending and their revenue subsegments.

Drilling down, our latest Behind the Numbers installment looks at the consumer portion of the above figures. How are consumer AR glasses expected to sell? What about apps, games, and experiences? And what will be the revenue models that develop around consumer headworn AR?

Headworn AR Global Revenue Forecast: 2024-2029

Common Pattern

Starting at the top, global consumer headworn AR spending is projected to grow from U.S. $935 million in 2024 to U.S. $8.2 billion in 2029, a 54.36 percent CAGR. This rapid growth is driven by competing road maps of tech giants releasing AR glasses in the next few years.

Subcategories of the above spending figures include AR glasses (see the table below for device inclusions), and the apps & experiences that run on those devices. Like many tech products, hardware comes first and leads in revenue share, which is then outpaced by software spend.

This happens as a larger installed base of in-market hardware accumulates, and as software – with faster refresh cycles – revenue per user (ARPU) grows. This is a common pattern for consumer technology, as seen historically with smartphone hardware and software (app) sales.

As for software revenue models, they’ll be defined by Apple, Meta, Google (Android XR), Snap, and others as they compete for consumer AR market share. This market is heating up around the success of low-immersion smart glasses, such as Ray-Ban Meta Smartglasses (RBMS).

A few of the above players – especially Google – have been somewhat frenetic in their XR strategies over the past decade. But with validated demand due to Meta’s work with smart glasses, they’re now coalescing around strategies that involve similar “lite AR” approaches.

Landmark Moment

While that lite-AR development is underway – involving flat-AR and non-display AI glasses – the above players are developing longer-term strategies around dimensional AR glasses. These include Meta Orion, currently in prototype stages, as well as Snap consumer spectacles.

The latter could be a landmark moment for the AR industry and for Snap. Consumer Spectacles will enter the market uncontested for consumer-geared dimensional AR glasses. There are dimensional AR glasses in the market, such as Magic Leap 2, but they’re enterprise-focused.

So 2026 could be a telling moment for consumer demand and temperature for full-fledged AR glasses. We currently don’t have much precedent by which to devise an addressable market, so Snap’s introduction of Spectacles in 2026 will be an important trial balloon for the AR industry.

Meanwhile, back to the software side of things, apps and use cases will follow the above hardware moves, including entertainment, communications, and commerce. Revenue models will develop around these use cases, including subscriptions, premium content, and ad monetization.

Some of the above will be housed in the app stores that are anchored to the platforms – with Apple, Google, Meta, Snap, and others competing aggressively for the ultimate consumer AR touchpoint. This could develop quickly, judging by the near-term AR road maps of these players.

We’ll pause there and circle back in the next Behind the Numbers installment with more numbers & narratives. Meanwhile, check out the full report.