Though smartphones dominate AR today – based mostly on a massive installed base – the technology’s fully-actualized form is headworn. But AR glasses are still years from ubiquity, as the underlying technology isn’t to the point of achieving both stylistic-viability and robust UX.

Of course, the previous statement applies more to consumer markets, as style isn’t as big an issue in the enterprise. And that principle is playing out today as enterprise AR spending far exceeds its consumer counterpart, as our research arm ARtillery Intelligence recently quantified.

But that consumer/enterprise split could flip in the coming decade, as consumer markets are inherently larger than enterprise ones. That will happen as the underlying technology improves and slims down; and as the industry’s ultimate wild card is played: Apple Glass.

To break down all of the above — including Apple AR discourse — and to dive deeper on the latest figures, ARtillery Chief Analyst Mike Boland recently gave a virtual-event presentation. We’re featuring it for this week’s XR Talks, including embedded video and narrative takeways below.

By the Numbers

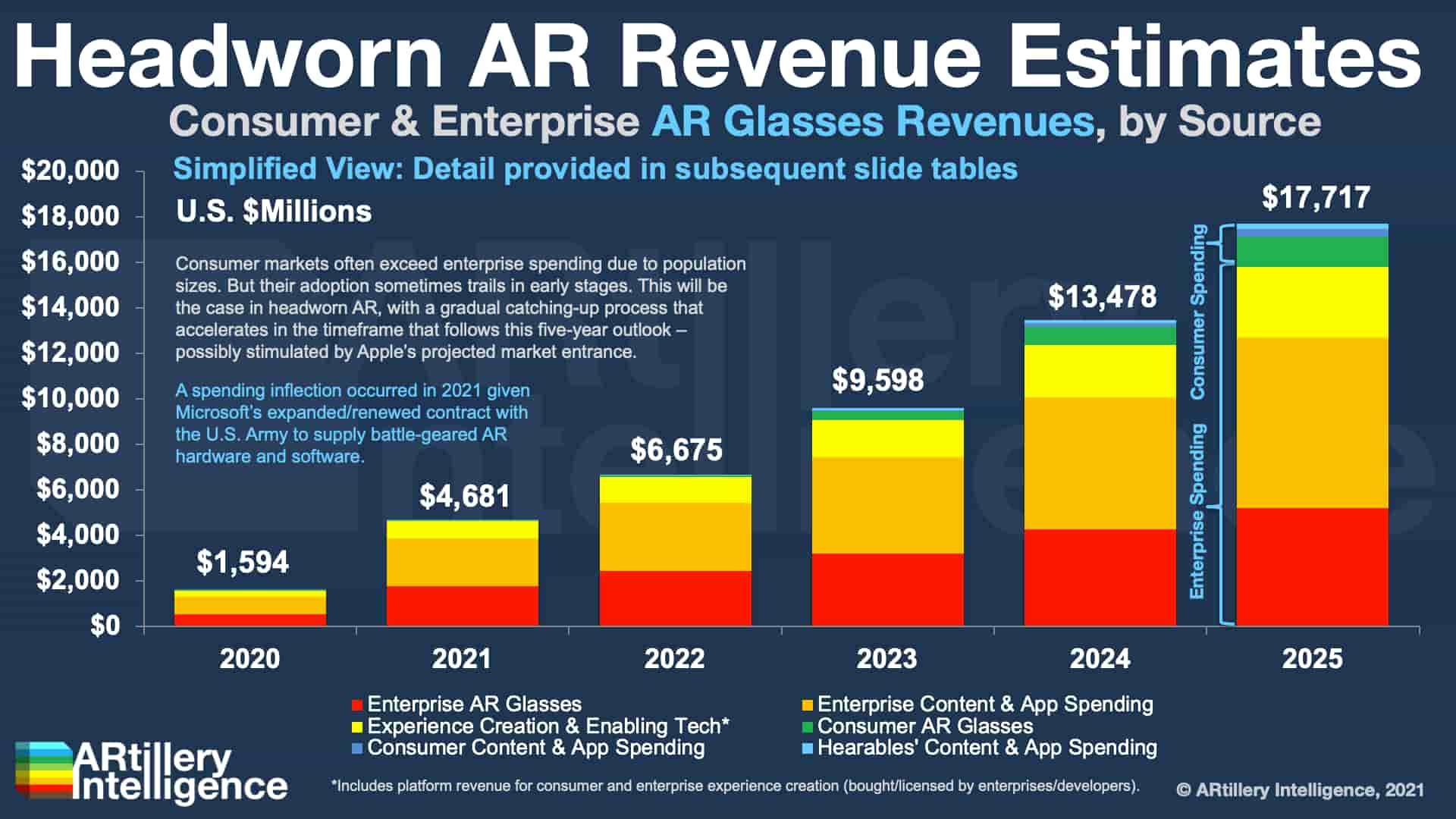

Jumping right into the numbers, headworn AR revenue is projected to grow from $1.6 billion in 2020 to almost $18 billion by 2025. That consists of several revenue subsegments including consumer, enterprise, hardware, software and various combinations of these factors.

As noted above, enterprise has the lion’s share of AR glasses spending today. But over time, the consumer spending share will catch up. That will take a while to happen but the longer-term outlook (beyond this five-year forecast) is for consumer AR spending to eclipse enterprise.

Breaking things down further, enterprise spending is not only greater but more complex. It’s subdivided by spending on enterprise-deployed AR headsets and software, as well as B2B enabling tech. The latter includes things like AR authoring and experience-creation software.

It’s also worth noting that enterprise AR’s spending lead is accelerated by the U.S. Army’s $22 billion 10-year contract with Microsoft to supply battle-grade Hololens units. This caused enterprise AR spending to inflect in 2021, though there’s still healthy growth for other headsets.

The Foundation

Moving on to consumer AR glasses, the foundation for the revenue opportunity is the hardware installed base. There, AR glasses are projected to grow from an almost non-existent base today to a projected 2.1 million units in 2025, mostly led by Apple after it enters the market.

When looking at Apple’s projected unit sales, estimates follow historical growth patterns in early (and initially underwhelming) Apple products such as Watch and Airpods. Those products took a few years to ramp up, and the cultural acceptance of smart glasses could take even longer.

Beyond annual unit sales, if we look at cumulative installed base – quantifying the number of headsets in market at any given time – it’s projected to reach about 4 million units by 2025. That’s steep growth, (see below) as installed base figures accelerate faster than annual unit sales.

But to put that growth into perspective, we can compare it to a known quantity in today’s market: smartphones. If we look at that 4 million units in 2025 relative to the smartphone installed base, it’s dwarfed by a magnitude of 879 to 1. So AR glasses have a long road to ubiquity.

Meaningful Impact

Drilling down on Apple, its market entrance will clearly have a meaningful impact on the aggregate health of the consumer AR sector. Given that so much is riding on that, a key question is what will Apple Glass – as it’s rumored to be called – look like? What will it be and do?

Several clues point to the fact that Apple won’t launch AR glasses — at least in V1 — that employ advanced AR. By that, we mean world-immersive AR that has spatial and semantic understanding of its surroundings: graphics overlay the world in dimensionally-accurate (SLAM) ways.

To achieve these functions, there are design tradeoffs such as bulk and heat, which would deviate from Apple’s style and design sensibilities. So in the sliding scale between sleeker “lite AR” glasses and bulky “heavy AR” (think: HoloLens), Apple will likely lean towards the former.

What will that look like? V1 could be more of a heads-up display (HUD). But though that represents a more rudimentary (and underwhelming) form of AR, Apple will counterbalance that with a more meaningful overall experience, including elegant integration with other Apple devices.

For example, we could see spatial audio integration with AirPods and notifications from your Apple Watch and iPhone. Though visuals won’t be immersive, slick integrations and experiences will drive the device’s appeal. And this fits the profile for Apple’s classic ecosystem playbook.

Starting Point

What evidence supports the above? One clue is the state of the underlying technology. It’s not to the point where wearability and graphical intensity are possible in the same device. The second clue comes from Apple’s size and resulting fiduciary drive to pursue massive markets.

Picking up on the second point, “lite AR” glasses have a much larger potential market, as “heavy AR” only appeals to a subset of technophiles. Apple’s mass-market requirements could lead it to AR hardware that is more along the lines of corrective eyewear or sunglasses.

In other words, eyeglasses and sunglasses are much larger markets than AR glasses – to the tune of about $200 billion. This is a much larger payoff, as Apple learned in positioning its other breakout-success wearables in massive markets such as earphones and watches.

Meanwhile, “lite AR” could be the starting point for Apple’s looming era of sensory augmentation. It could then gain levels of immersion and graphical richness over several years….just like the iPhone 1’s evolutionary path towards the pocket supercomputer we know today.

But that won’t happen overnight. We often forget the iPhone 1 only sold a few million units and didn’t reach the 100 million magic number until the iPhone 4. Whatever Apple launches, we should temper expectations about immediate game-changing impact. That will be a long process.

We’ll pause there and cue the full video below…