Data Point of the Week is AR Insider’s weekly dive into data from around the XR universe. Spanning usage and market-sizing data, it’s meant to draw insights for XR players or would-be entrants. To see an indexed archive of data briefs and slide bank, subscribe to ARtillery Pro.

In the wake of last week’s Snapchat announcements around new AR features, there’s lots of evidence that social use cases lead consumer AR market share. And that works on several levels including number of active users (key word: active), time spent and most of all, revenue.

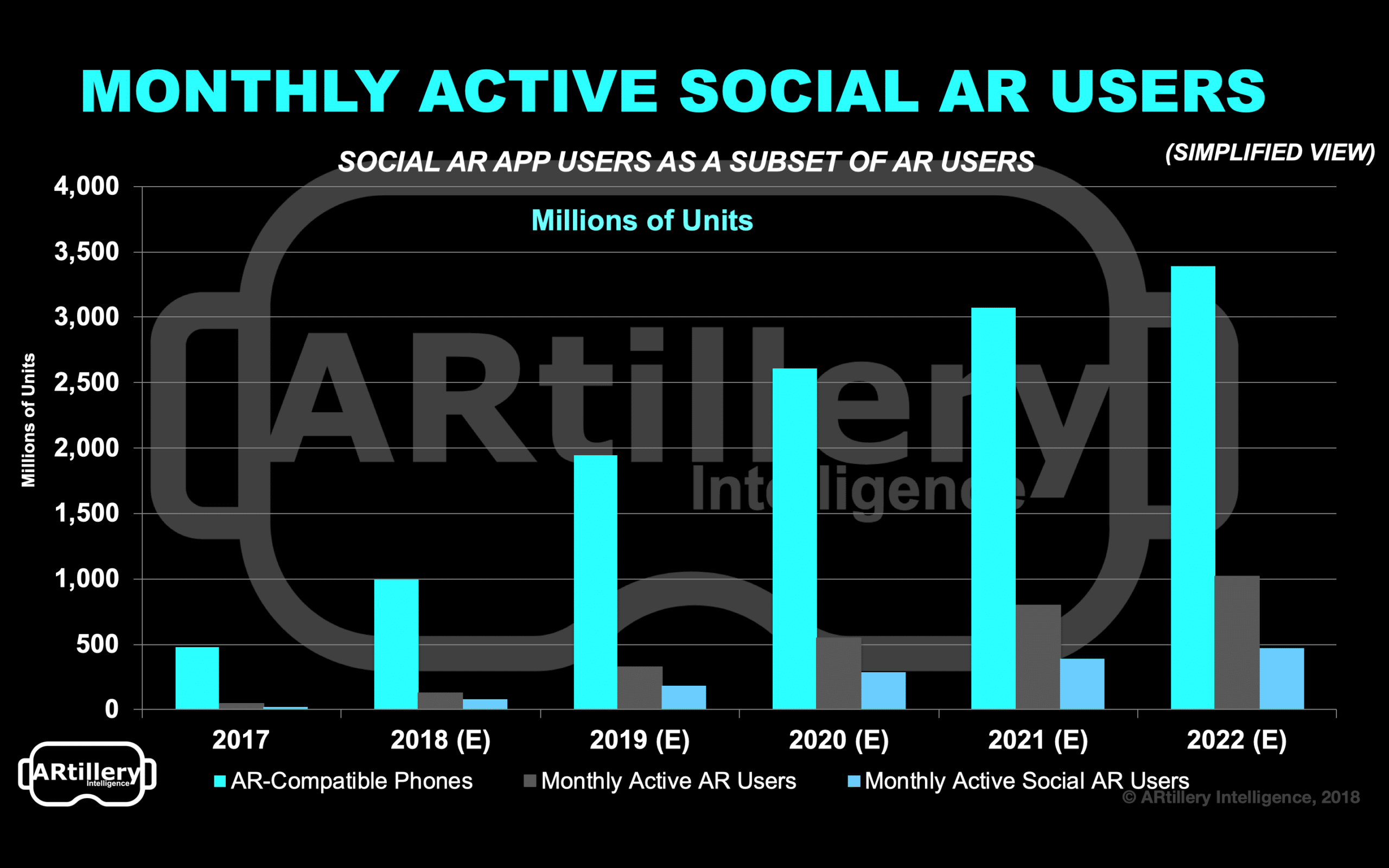

For active users, Snapchat reported at last week’s Partner Summit that 70 percent of its 186 million daily users activate AR lenses daily, and 15 billion have been viewed to date. By comparison, the other AR leader, Pokemon Go, has roughly 65 million monthly active users.

But there’s a key distinction: AR’s role in Pokemon Go isn’t primary, whereas it’s certainly a central experiential component of AR lenses. For Pokemon Go, AR is an element of play, but one that most users de-activate due to battery drain or difficulty levels (more on that in a bit.).

This distinction enters the revenue picture too. People (including us) point to Pokemon Go’s $2.3 billion in cumulative in-app-purchase revenues. But all of that revenue isn’t directly attributable to AR for the reasons mentioned above, whereas Snap’s branded lens revenue is all AR.

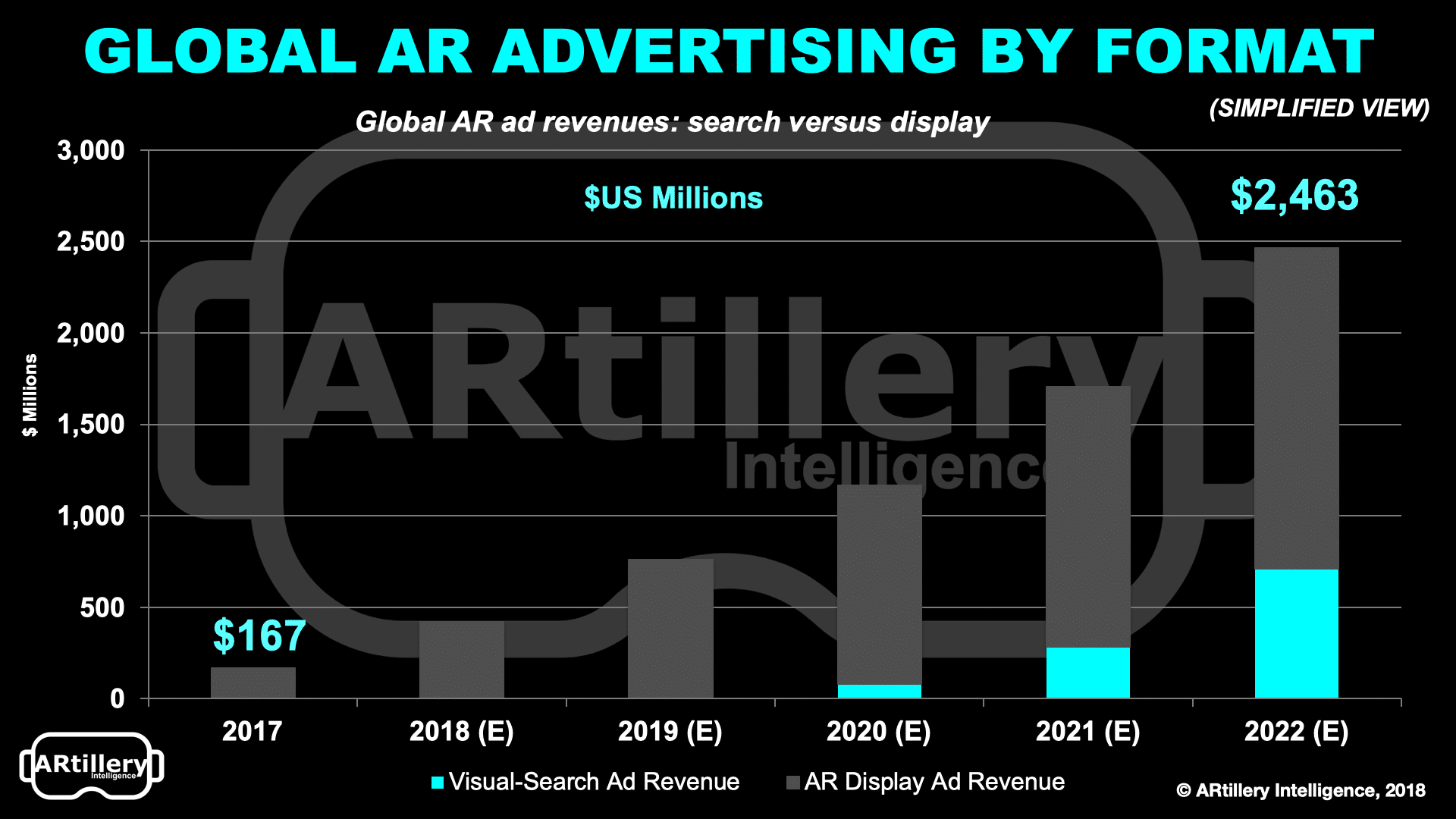

We’ve projected that Snap derived $236 million of the $408 million spent on AR advertising in 2018. The total ad spend from social lenses is projected to reach $2.4 billion by 2022. It’s the leading AR revenue category today, if you don’t count Pokemon Go’s in-app-purchases.

That brings up another key distinction. With social lenses, the revenue source is brands that apply ad budget (advertiser pays) to this emerging and immersive form of customer engagement. Pokemon Go rather follows the mobile gaming playbook with in-app-purchases (user pays).

As for whether or not Pokemon Go should be counted in AR figures and considered an AR experience, that’s an age-old question (in AR years). On micro levels, it’s not really AR for the reasons cited above. But if we broaden the definition of “augmentation,” it sort of is.

In other words, on a pixel (or voxel) level it’s not AR in lots of ways (scene mapping, etc.), though that’s improving. But on a contextual level, the experience is augmented with situational awareness. For example, certain Pokemon are found in certain landscapes, (think: near water).

There are legitimate arguments on both sides. App analytics firms like Sensor Tower don’t count Pokemon Go in their AR app tallies. But that’s more because they don’t include AR experiences in non-AR apps (AR-as-a-feature), which also incidentally includes social AR lenses.

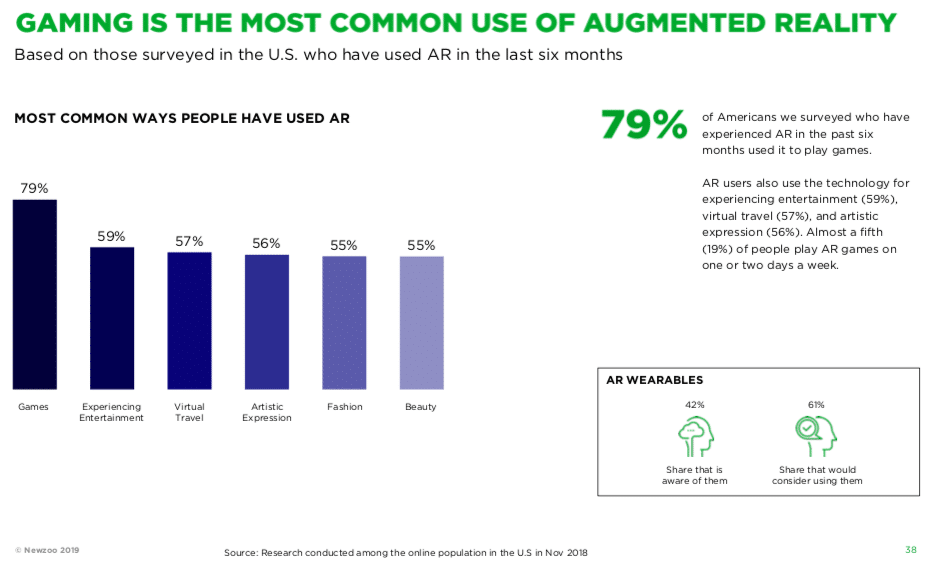

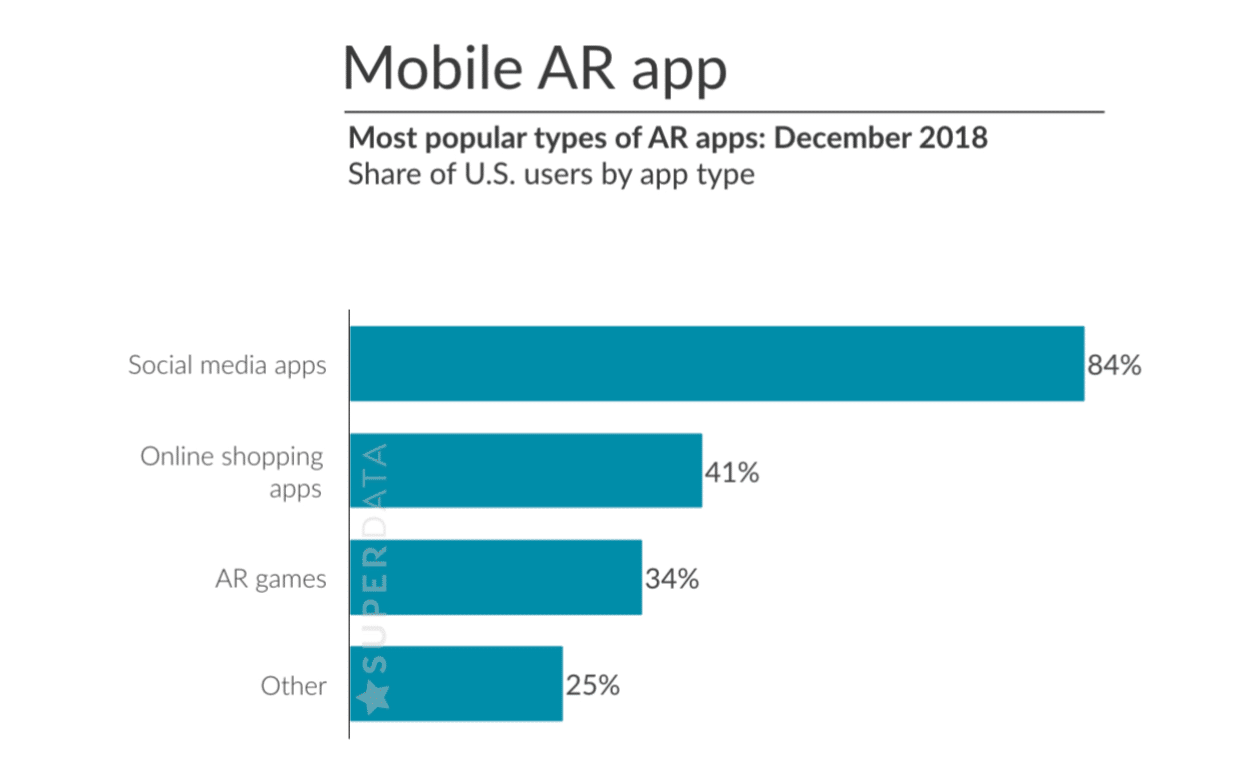

The same goes for research firms. ARtillery Intelligence counts Pokemon Go in consumer AR survey data. NewZoo does the same, but SuperData doesn’t appear to. There’s no wrong answer, as long as definitions, inclusions and methodology are explicit and well-reasoned.

We’ll be back with a deeper dive on Pokemon Go’s AR “status” and the concept of broadening the definition of augmentation. That includes hearables and other things that break out of the graphically-bound definition of AR. The good news: that outlook broadens the market opportunity.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.