This post is adapted from ARtillery Intelligence’s report, Mobile AR Strategies & Business Models. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

In AR’s early stages, a common question continues to be asked: where’s the money? There have been oscillations in excitement and doubt over AR, but the ultimate proof point will be revenue. Though aggregate revenues have disappointed, there are segments that are bearing fruit.

So we’ve determined the three biggest revenue categories for consumer-based mobile AR. We’ve examined them on qualitative and quantitative levels. The former entails product models, leading companies and best practices. The latter entails market sizing and revenue projections.

But before we dive into these models, starting today with advertising, what are they at a high level? We categorize them as follows:

1. Advertising (brands pay)

2. In-app purchases (consumers pay)

3. AR-as-a-service (enterprises pay)

Unpacking IAP

Second on our list of consumer AR software business models is In-App Purchases (IAP). This category has Pokémon Go to thank for its prominence and inclusion in this report. The location-based AR game has derived an estimated $3 billion in IAP revenue to date.

Further validating IAP is the fact that it’s an established revenue model in mobile gaming – the same soil from which AR gaming sprouts. That means consumers are already acclimated to IAP. Premium apps are conversely untenable for AR because the technology is too early and unproven.

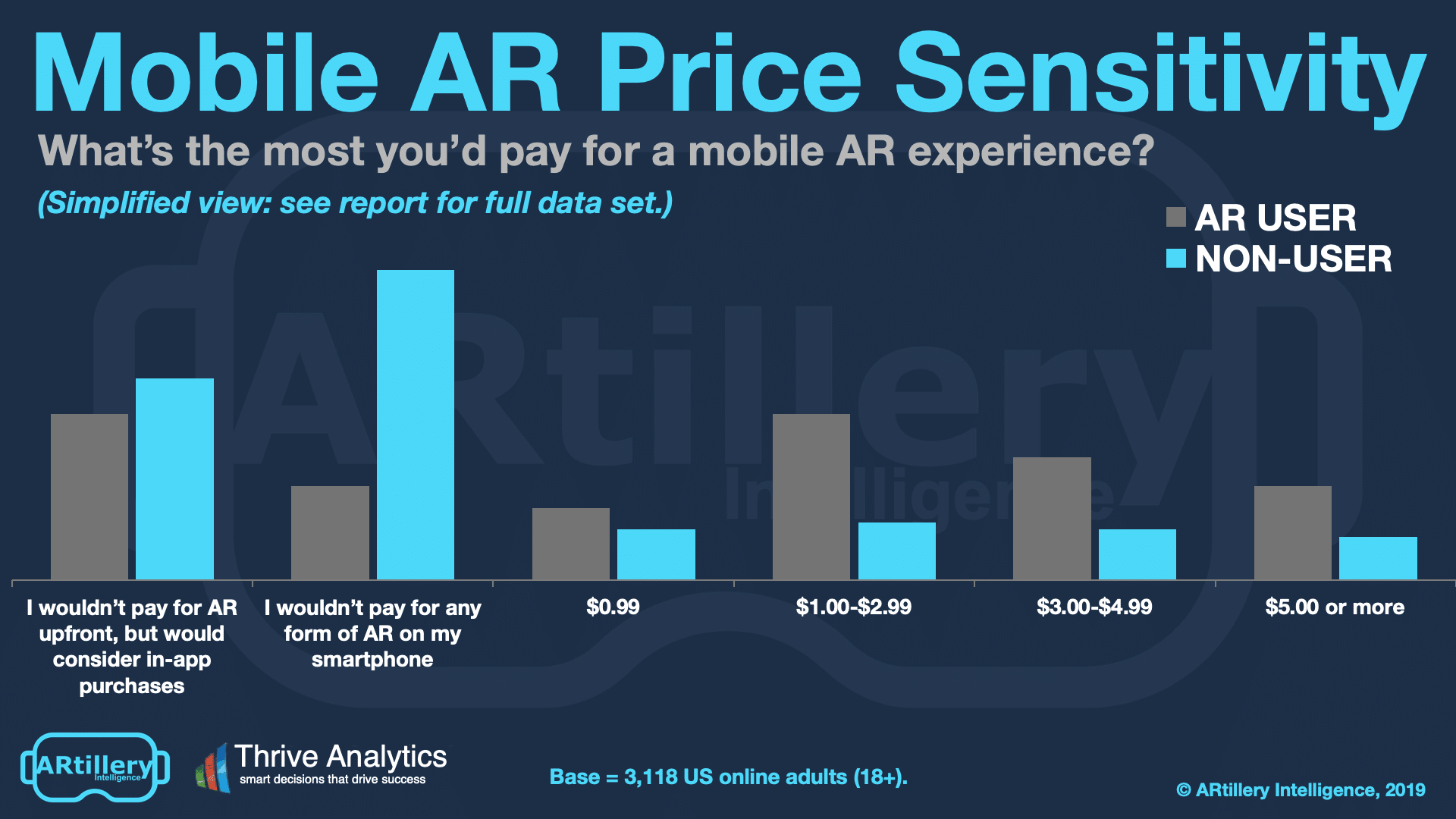

This notion is supported by ARtillery Intelligence’s consumer survey data with Thrive Analytics (see below). IAP is the most popular payment option among survey respondents. Along with the above evidence, this is a strong signal for IAP’s strength as a near-term AR revenue model.

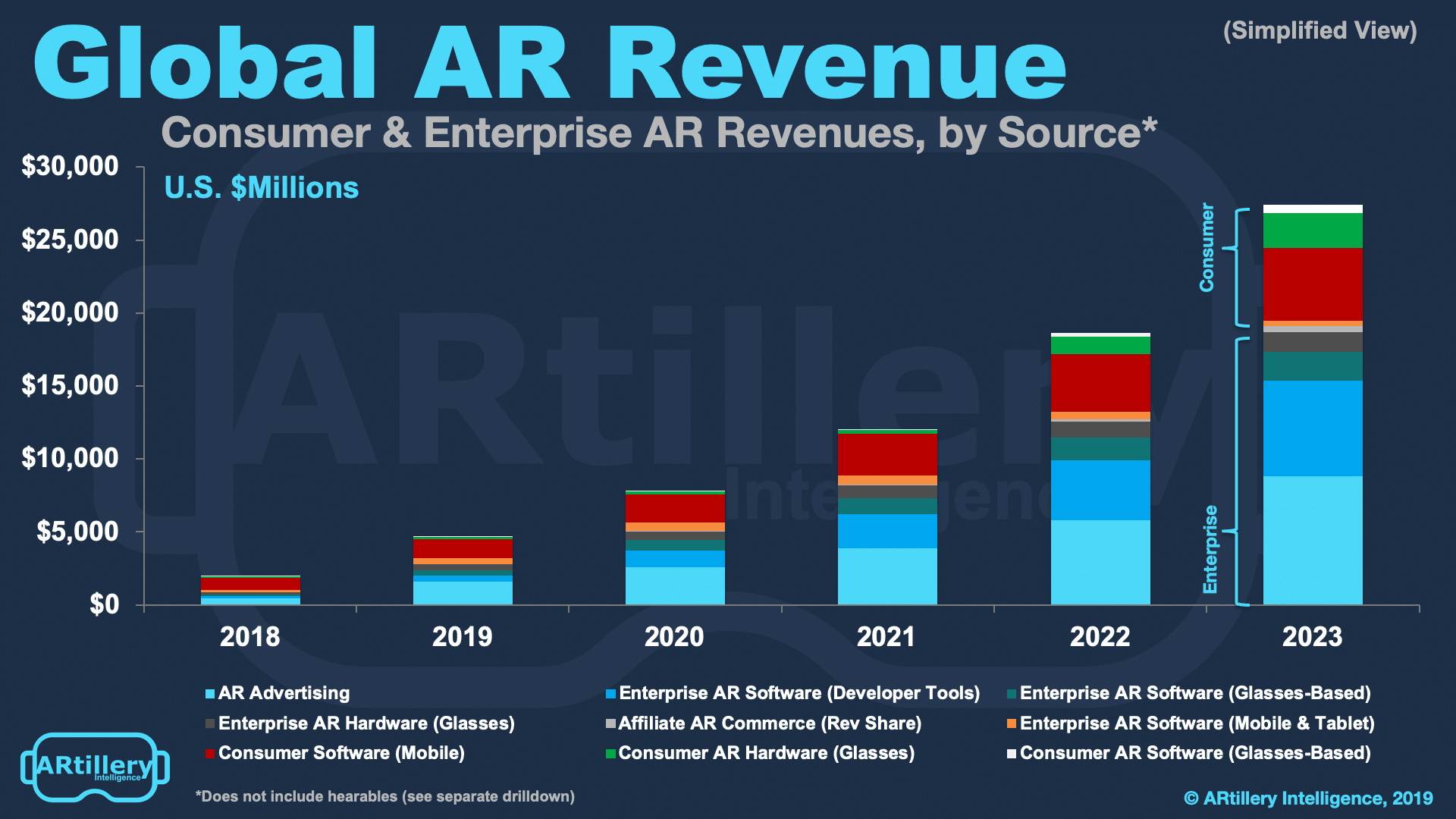

Based on these and other signals, ARtillery Intelligence has an optimistic outlook for IAP in its market sizing. In its Global AR Revenue Forecast, IAP is a leading revenue source among AR sub-sectors (see above). It’s projected to grow from $863 million in 2018 to $4.9 billion by 2023.

Beyond the quantitative assessment, what’s the qualitative view on IAP? Who’s showing best practices and what are the ways it will materialize in the coming months and years? The answer is mostly “Pokémon Go.” As the leader in AR gaming, there are several things it can teach us.

Lessons From Pokémon Go

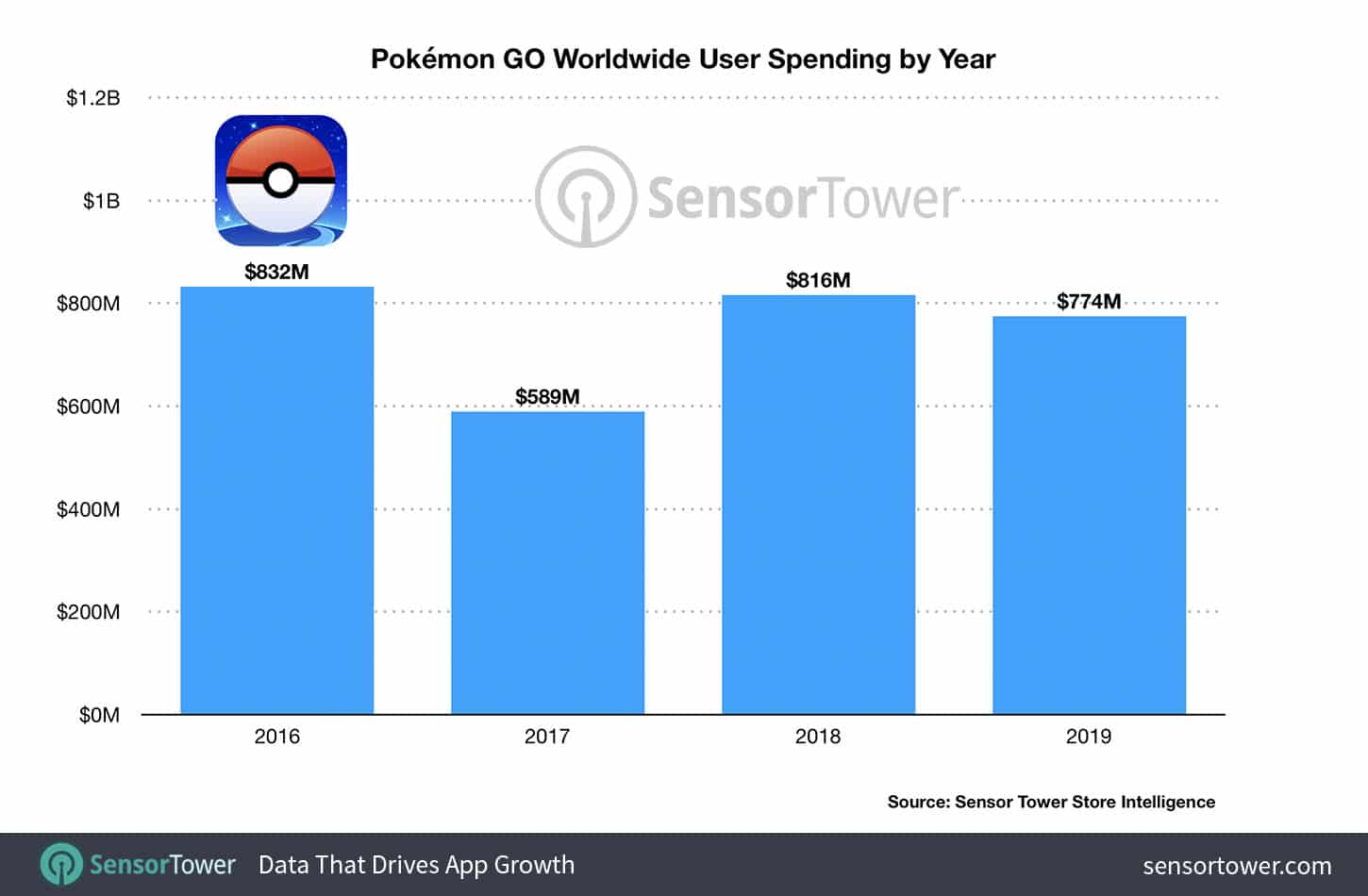

As we passed Pokémon Go’s third birthday in July, evidence emerged of its lifetime revenue. Sensor Tower estimated total revenues of $2.65 billion, which it since updated to $3 billion last month. This notably ranks the game ahead of Candy Crush and Clash Royale – a sizable feat.

Further putting things in perspective, estimated 2019 year-to-date gross revenue is $774 million, which puts it mostly on pace with 2018 revenue. Daily average revenue since launch is $2.4 million, and its average revenue per player (ARPU) is $5, corresponding to 521 million downloads.

But these are cumulative figures. What about the present? Despite falling from its Q3 2016 peak Pokémon Go has resurged in 2019. In fact, August 2019 was its biggest revenue month in three years and fourth-largest to date with $110 million in revenue according to Sensor Tower.

One lesson from this is that Pokémon Go’s usage and revenue have mostly sustained over time. This is rare for mobile games, given common play cycles. Games quickly lose novelty and their mechanics have to be refreshed to maintain competitive appeal among accomplished players.

So what has Pokémon Go done to counteract these forces? There are several answers including updating Pokémon in deliberate intervals to keep game challenges and accomplishments fresh. For example, its August surge is attributed to incorporating “Team Rocket” into gameplay.

Native Fit

Another feature Niantic added in 2019 is a sort of fitness tracker. It tracks and gamifies players’ steps in the background, which adds new dimensions of play and competitiveness. It’s also “on-brand” and aligned with game maker Niantic’s core mission to get people out of the house.

Niantic has also been successful in limiting AR to a feature rather than a primary function. Due to its new and unproven status, it’s smart to ease users into AR. It also added AR where it natively fit, such as a feature that lets players pose with captured Pokémon for social shares.

These tactics join the underlying advantages such as strong IP and smart game mechanics. For example, the game balances challenging play with attainable accomplishments. And though the game is technically asynchronous (one-player), it’s conducive to group outings and social activity.

We’ll be back next week to continue the discussion around in-app purchases, including Harry Potter, Wizards Unite and Minecraft Earth. Meanwhile, see more about this report or subscribe to access it here. Revenue models will be a quickly moving target as AR finds its footing.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.