Data Dive is AR Insider’s weekly dive into the latest spatial computing figures. Running Mondays, it includes data points, narrative insights and takeaways. For an indexed library of data, reports, and multimedia, subscribe to ARtillery Pro.

Wearables continue to be one of the fastest-growing product categories in consumer tech. This is notable given that all-things hardware are constrained during Covid-era lockdowns. Those headwinds result from both supply-chain impediments and consumer-spending slowdowns.

This is indirectly but importantly relevant to AR. As we continue to examine, wearables are AR’s forbear, in that they will condition consumers to wear sensors on their bodies. That could eventually ease the cultural and stylistic acclimation to AR glasses, which will be an uphill battle.

Meanwhile, wearables are further propelled by tech-giant motivations. That’s especially true for Apple, which continues to double down on Watch and AirPods. It sees wearables both offsetting near-term iPhone revenue deceleration; and future-proofing its hardware-heavy profit machine.

As we’ve examined, Watch and Airpods could eventually converge with glasses in a holistic suite that augments reality from several angles. This could replace (or augment) the current suite of iThings, which notably fits the profile for Apple’s ARPU-driving multi-device ecosystem approach.

True Test

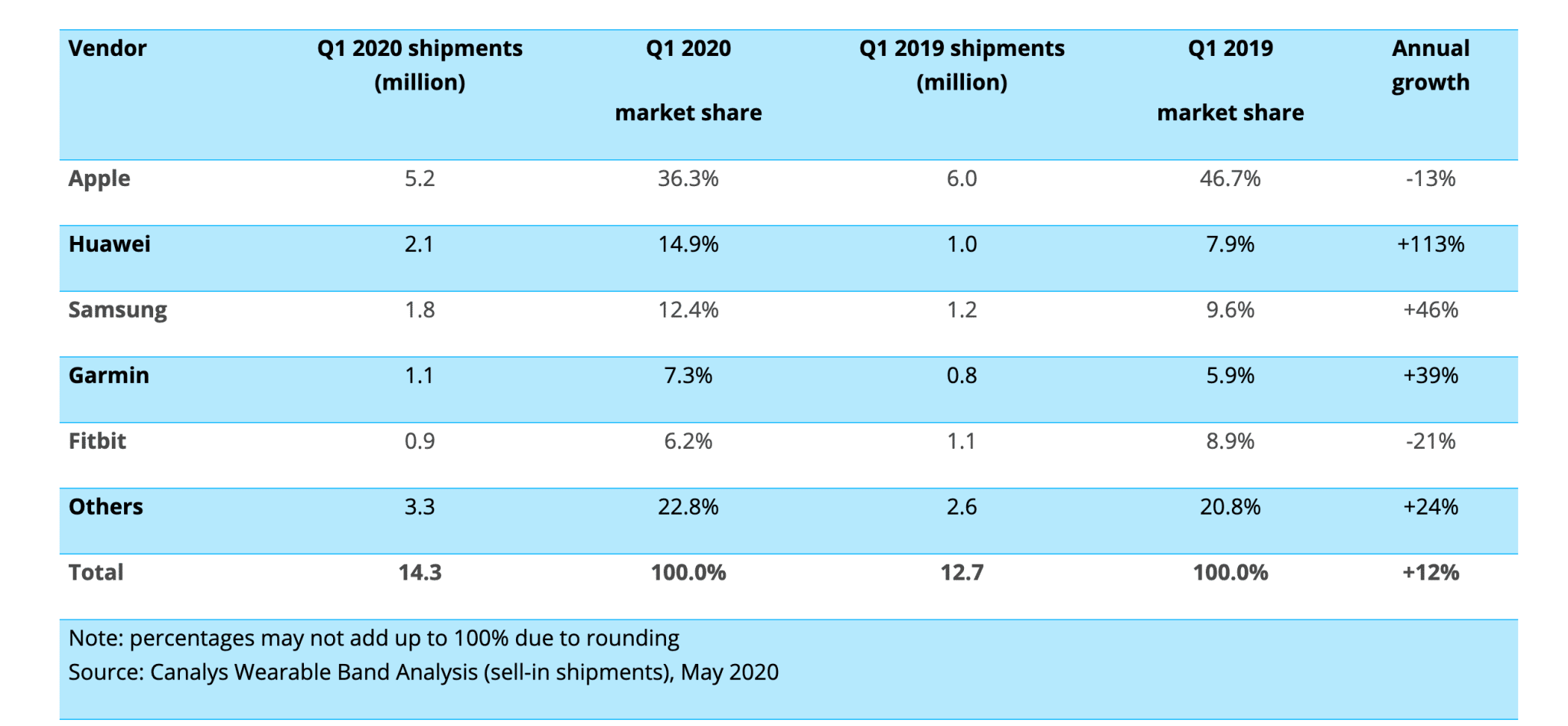

With that backdrop, the latest proof point for wearables growth and resilience comes from Canalys’ smartwatch tracking. It reports that unit shipments grew 12 percent year-over-year in Q1, up to 14.3 million (see above). This comes despite pandemic-incited economic slowdowns.

In fairness, any Covid-led Q1 impact would be limited to March. And economic fallout is a trailing indicator in this case. So the true test will come with Q2 figures. But optimism flows from expected wearables inflections that are tied to quarantine-driven fitness and health-tracking.

Canalys’ figures directionally align with Strategy Analytics, which reports 20 percent year-over-year smartwatch growth, reaching 13.7 million units in Q1. The firm logically expects shipments to decline in Q2 but then recover in the second half of 2020, ending in an annual net positive.

ABI Research has a similar take, projecting that wearables unit shipments (beyond just smartwatches) will be up 5 percent in 2020. Though this signals growth in the face of a pandemic, it should be noted that it’s been adjusted from the 17 percent rise previously projected.

Succession Plan

One common thread between all of the above estimates — besides aggregate wearables growth — is Apple’s leading market share. For example, Strategy Analytics pegs Apple’s Q1 smartwatch market share at 55 percent, followed by Samsung (14 percent) and Garmin (8 percent).

That brings us back to Apple and the earlier claim that it’s doubling down on wearables in the ongoing feedback loop emitted from the category’s success. Among other things, wearables are offsetting the continued revenue deceleration in Cupertino’s prized pig, the iPhone.

To validate that, we can go straight to the source. Apple’s fiscal Q2 (calendar Q1) earnings show “wearables, home and accessories” revenue growing 24 percent ($1.2 billion), while iPhone sales fell 6.7 percent ($2.1 billion). The former doesn’t fully redeem the latter, but the offset is valued.

As noted, this revenue reconciliation is just one task that wearables have at Apple. The other is to buttress the iPhone succession plan, where Apple has a lot riding. There won’t be a single iPhone replacement but an iPhone-dependent wearables suite — including glasses — is likely.

Header Image Credit: Apple