Industry rhetoric about AR’s world-changing status sometimes outweighs evidence that it’s captivating consumers today. Though we see some signals, such as lens engagement figures from Snap and others, we’re often “flying blind” when it comes to consumer AR sentiment.

Looking to fill that gap, AR Insider’s research arm ARtillery Intelligence has completed Wave V of its annual consumer survey report. Working with consumer survey specialist Thrive Analytics, it wrote questions to be fielded to 102,000+ U.S. adults and produced a report based on the results.

Known as AR Usage & Consumer Attitudes, Wave V, it follows similar reports over the last few years. Five waves of research now bring new insights and trend data to light. And all five waves represent a collective six-digit sum of U.S. adults for robust longitudinal analysis.

Among the topics: How is mobile AR resonating with everyday consumers? How often are they using it? How satisfied are they? What types of experiences do they like most? How much are they willing to pay for it? And for those who aren’t interested in mobile AR….why not?

Fun & Games

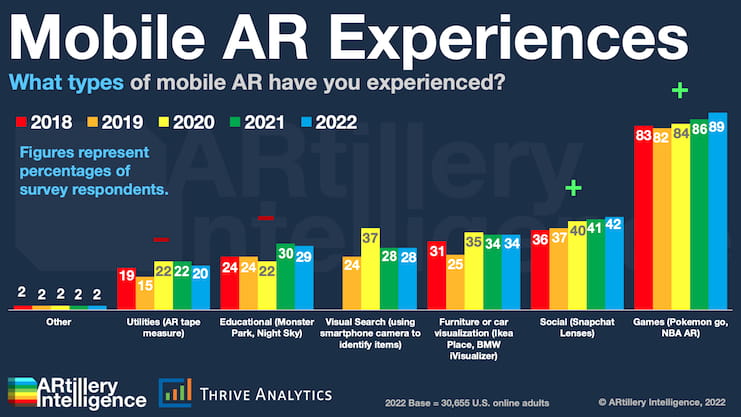

Picking up where we left off in the last installment, what content categories are mobile AR users consuming most? The most popular flavors of AR are Pokémon Go and Snapchat Lenses. So naturally, gaming (89 percent) and social (42 percent) lead our survey.

As a matter of methodology, we explicitly name these experiences as examples when asking survey respondents about the corresponding experience types. To avoid gray area and false positives in survey research, it’s always smart to use demonstrative language in questions.

While we’re at it, we’ll address another looming question: Is Pokémon Go AR? Many AR purists argue that it isn’t. Our take, examined in our report on Pokémon Go, is that any graphical, audible, or contextual augmentation of reality (the latter seen in Pokémon Go) constitutes AR.

As for specific success factors, Pokémon Go has an optimal mix of game mechanics, novel updates, challenging play, and real-world interaction. In fact, after receding from its 2016 peak, the game has quietly returned to high engagement levels and revenue performance.

As for social AR lenses, success factors include simple activation and shareability. There’s also a fun element, amplified by social-graph driven network effect and virality. This has caused Snap to exceed 250 million daily AR users and strong revenue growth from paid AR lenses.

Monetization Potential

Speaking of Snap, an ongoing goal is to boost its core products’ engagement and repeat use. It has seen that AR can not only accomplish this but can directly drive revenue. In the aggregate, AR ads drove an estimated $1.98 billion last year, growing to $6.68 billion in 2025.

Similarly, Google continues to invest in visual search to support and future-proof its core search business. As shown by Google Lens, users can point their phones at real-world items to contextualize them – a flavor of AR that deviates from the more popular social lenses.

Snap is similarly chasing this flavor of AR (Snap Scan) as is Pinterest (Pinterest Lens). Overall, we’re bullish on this form of AR. It carries a high-frequency use case that flows from its versatility and broad applicability… just like search itself…but with the physical world as its “index.”

For all these reasons, it’s surprising that visual search still lingers in fourth place in these survey results. But we’re still bulling on its future. The value of holding up one’s phone to contextualize real-world items will have wide appeal and, importantly, monetization potential over time.