This post is adapted from ARtillery Intelligence’s report, Mobile AR Strategies & Business Models. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

In AR’s early stages, a common question continues to be asked: where’s the money? There have been oscillations in excitement and doubt over AR, but the ultimate proof point will be revenue. Though aggregate revenues have disappointed, there are segments that are bearing fruit.

So we’ve determined the three biggest revenue categories for consumer-based mobile AR. We’ve examined them on qualitative and quantitative levels. The former entails product models, leading companies and best practices. The latter entails market sizing and revenue projections.

But before we dive into these models, continuing today with in-app purchases, what are they at a high level? We categorize them as follows:

1. Advertising (brands pay)

2. In-app purchases (consumers pay)

3. AR-as-a-service (enterprises pay)

Sizing up IAP

Second on our list of consumer AR software business models is In-App Purchases (IAP). This category has Pokémon Go to thank for its prominence and inclusion in this report. The location-based AR game recently exceeded an estimated $3 billion in cumulative IAP revenue to date.

Further validating IAP is the fact that it’s an established revenue model in mobile gaming – the same soil from which AR gaming sprouts. That means consumers are already acclimated to IAP. Premium apps are conversely untenable for AR because the technology is too early and unproven.

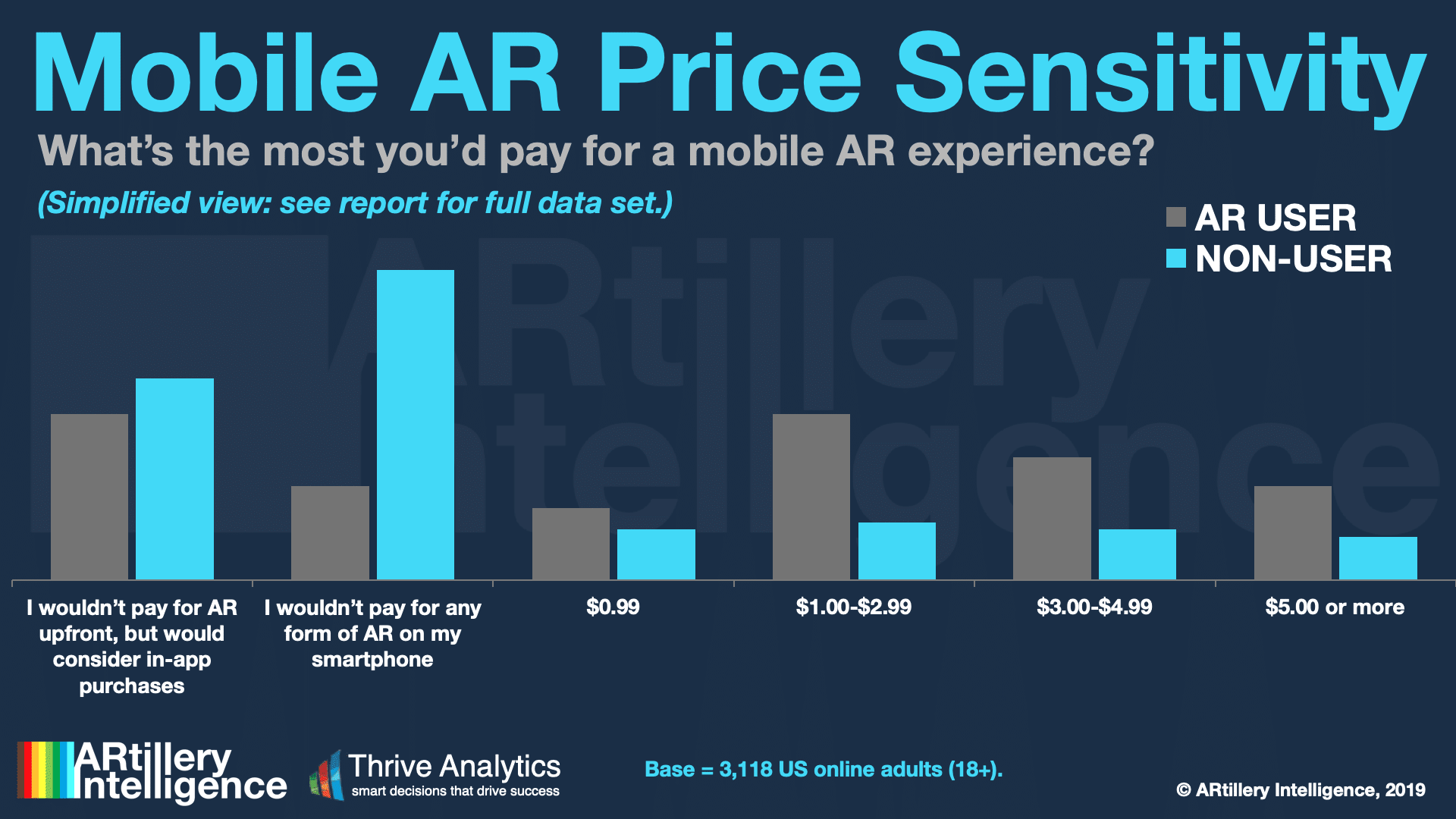

This notion is supported by ARtillery Intelligence’s consumer survey data with Thrive Analytics (see below). IAP is the most popular payment option among survey respondents. Along with the above evidence, this is a strong signal for IAP’s strength as a near-term AR revenue model.

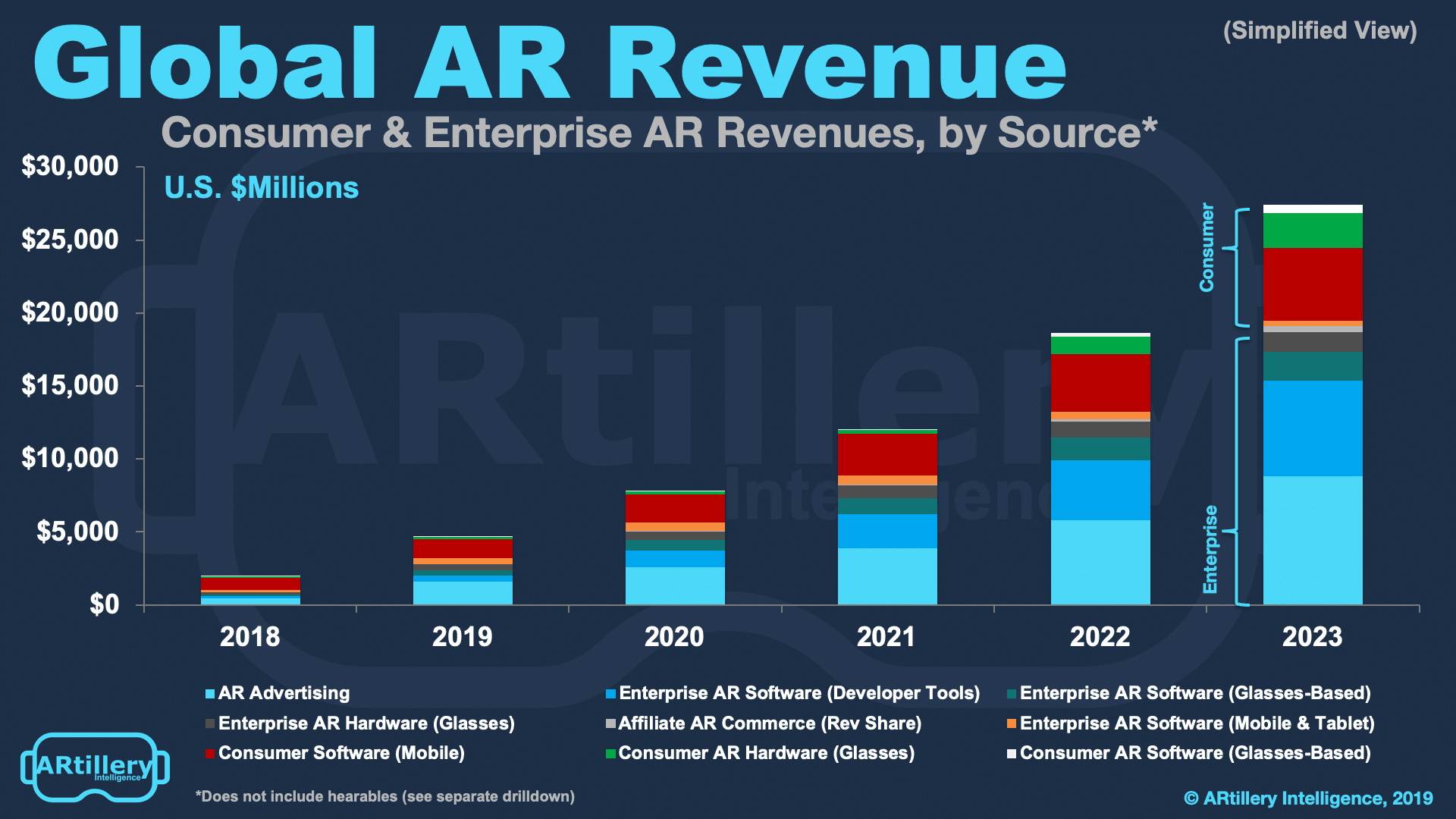

Based on these and other signals, ARtillery Intelligence has an optimistic outlook for IAP in its market sizing. In its Global AR Revenue Forecast, IAP is a leading revenue source among AR sub-sectors (see above). It’s projected to grow from $863 million in 2018 to $4.9 billion by 2023.

Beyond a quantitative assessment, what’s the qualitative view on IAP? Who’s showing best practices and how will it materialize in the coming years? The answer is mostly “Pokémon Go.” But after examining it in the last installment of this series, we turn attention to its successor.

Take Two: Harry Potter, Wizards Unite

Niantic’s follow up title, Harry Potter Wizards Unite has been hotly anticipated due to Pokémon Go’s success. Its performance so far involves bad news and good news. It’s tracking far behind Pokémon Go in usage and revenue… but it’s still a strong contender in its own right.

For example, it’s on pace to be the second highest-grossing location-based game of all time with $12 million in revenue in its first month. Though it’s pacing behind Pokémon Go, it exceeds other strong-IP titles in location-based AR such as Jurassic World Alive and Ghostbusters World.

As far as financial metrics, per-player spending (ARPU) during HPWU’s first month is $.46. That trails Pokemon Go’s $1.50 during the same period. But Pokémon Go’s lifetime ARPU rose to $5 in a cumulative timeframe, which indicates potential growth for HPWU as its momentum grows.

This begs the question of how other impending AR games will fare. Minecraft Go has lots of potential, given a massive engaged base of gen-Z players that demographically align with the camera-forward use case. It’s in the process of a slow rollout so we’ll have to wait and see.

Panning back further, there are interesting things happening in China (as always). Tencent’s Let’s Hunt Monsters has actually outperformed HPWU in revenue if you zero in on just iOS. And other location-based AR games will continue to develop, some with very strong IP.

Sticking to the earlier theme of bad news / good news, the bad news is that things are so early and undefined. The good news… things are so early and undefined. There will be lots of value creation as location-based AR gaming – and its revenue models – continue to grow into their own skin.

What’s Next for IAP?

Speaking of evolving paradigms, where else could IAP find a home. There are several areas that show potential, beyond experiences that fit the Pokémon Go mold. These signals mostly come from historical examples, such as successful models in non-AR mobile gaming.

The biggest of those is the revenue beast that is Fortnite. It has validated the fact that consumers will pay via in-app purchases and micro-transactions to personalize in-game characters. Not only is this validated in Fortnite but it’s theoretically well-aligned with AR’s current usage patterns.

For example, AR’s most popular modality measured in active users (even more so than Pokémon Go) is social lenses. These are all about self-expression and whimsical selfie fodder to share with friends. So far, these experiences are free, as they’re essentially subsidized by brand advertising.

That brings in a previous chapter of this report where brands are compelled to develop immersive product lenses as a marketing vehicle. Beyond those branded AR lenses, Snapchat and Facebook have seeded lens libraries with free community-created lenses to maximize their traction.

But once they reach a critical mass of traction and demand, Snapchat and Facebook could introduce consumer-pay options. The is what Snapchat did with Geofilters, where consumers, for a nominal fee, create and unlock a lens around a geofence and timeframe (think: birthday party).

Virtual Marketplace

IAP could accomplish a few things for Snap. It could unlock a long tail of consumer spending for AR lenses – sort of like advertisers do but higher-volume / lower-margin. It will also be another incentive to attract lens developers to its platform, given greater reach and monetization.

Longer-term, this will apply to more advanced forms of AR. AR Cloud innovator Ubiquity6 is keen on the idea of a marketplace for AR expression and personalization. It could sit between creators, users and experience curators as a platform, collecting affiliate fees for digital transactions.

Other players such as Aura want to build an “avatar as a service.” This will be a turnkey avatar creation engine that AR game developers integrate. They can then share revenue for in-app purchases as players personalize avatars a la Fortnite. It could be a sizable AR revenue category.

We’ll be circle back soon to continue this discussion around top consumer AR revenue models. Next we’ll cover “AR as a Service.” Meanwhile, see more about this report or subscribe to access it here. Revenue models will be a quickly moving target as AR finds its footing.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.