Through oscillations of excitement and doubt in AR, what are the market factors that indicate its growth potential? These “confidence signals” as we call them were the topic of our recent presentation at AWE Nite SF (video below).

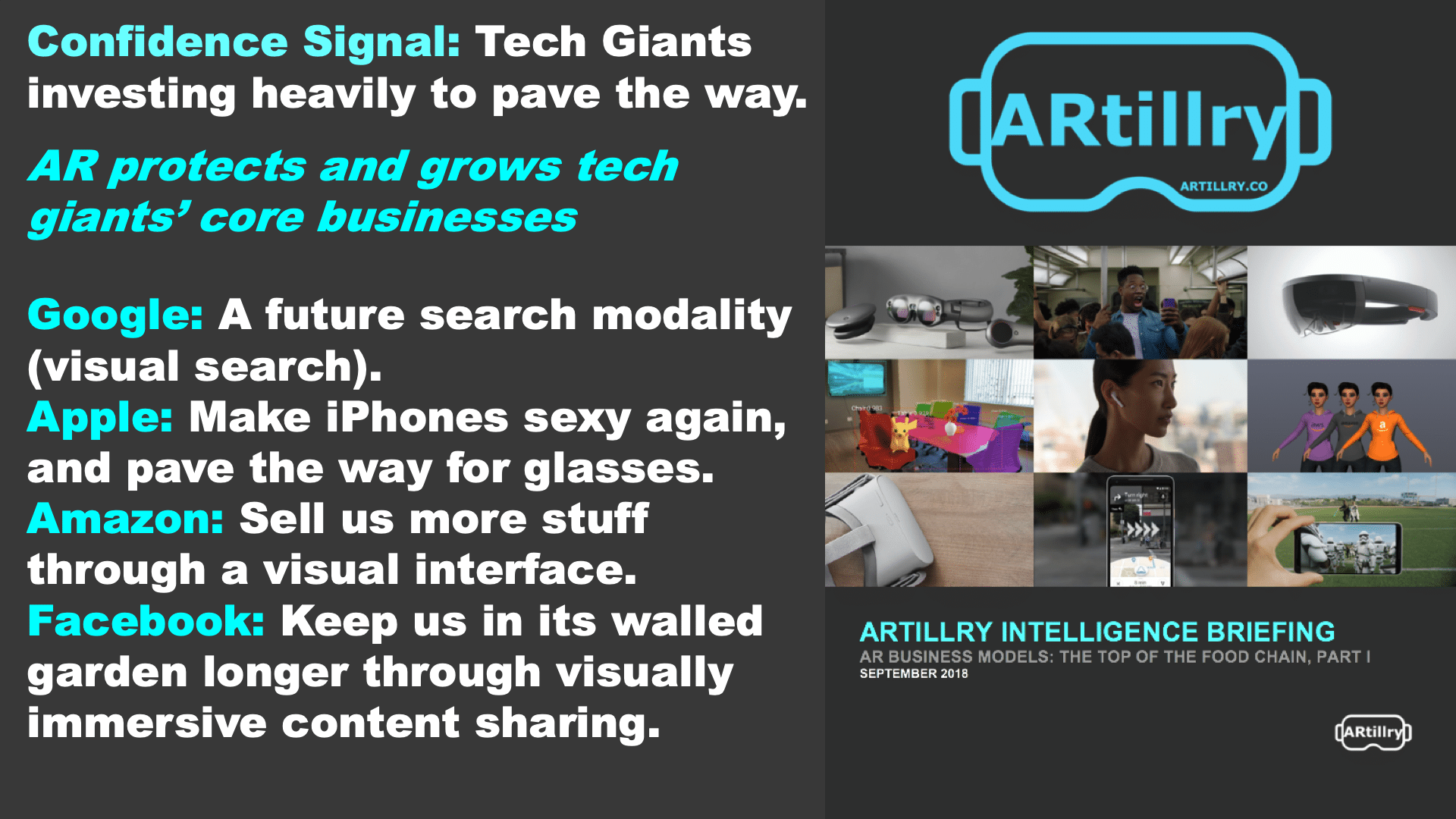

One of the biggest confidence signals for example is to “follow the money.” Billions being invested by tech giants not only indicates a future for AR, but what that future could look like. Through self-interested positioning, they’re building platforms and paving the roads for the rest the sector.

For example, Google has a vested interest AR-based visual search to boost monetizable search query volume. Facebook wants to keep us in its walled garden through visually-immersive content sharing like AR lenses. Branded lenses also directly monetize through product try-ons.

Apple meanwhile wants to make the maturing iPhone sexy again through AR, while also planting the seeds for a longer-term AR hardware suite (glasses, hearables, etc.). And Amazon has AR features that let shoppers visualize products in-home to boost e-commerce and reduce returns.

Historical Lessons

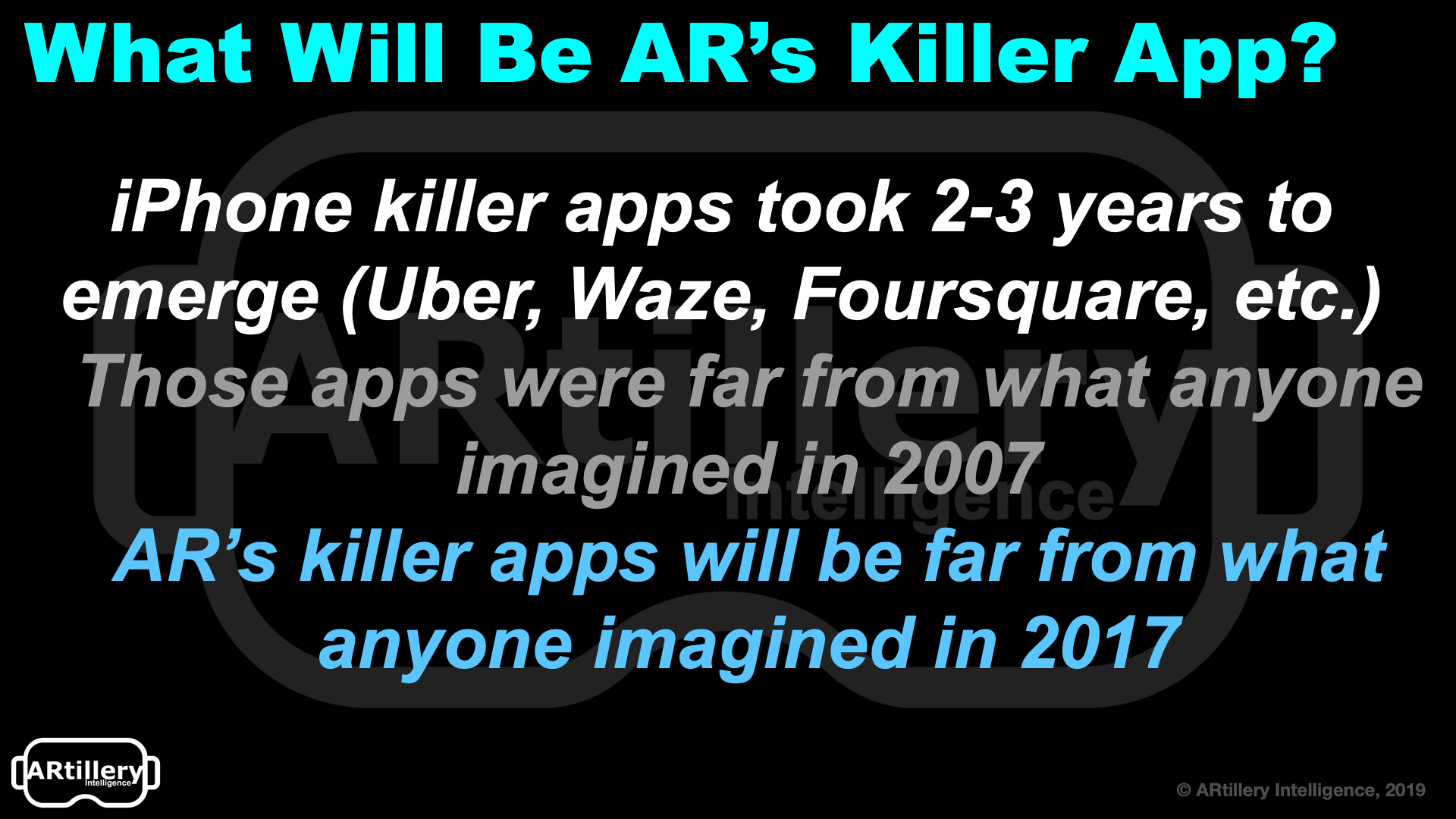

But that still leaves the question of what AR’s killer app will be. The AR sector has gotten flak for not producing a mass-market killer app. Pokemon Go and Snapchat Lenses have certainly reached killer app-like penetration. But for world-immersive AR, we’re not there yet.

But the question is whether or not that’s a bad thing. Does AR need a killer app yet? Looking to historical evidence — our favorite pastime — iPhone killer apps didn’t arrive until 2-3 years after the device’s introduction. 2-3 years from ARkit’s June 2017 launch is later this year, or next year.

Like with the iPhone, this is the requisite incubation period for developers to gain their native footing. We’re otherwise anchored to the mentality of legacy technology. At the time of the iPhone’s 2007 launch, that meant a desktop mentality. Today, it means a mobile 2D mentality.

So when will AR’s killer apps arrive? It won’t exactly follow the 2-3 year incubation cycle we saw with those early iPhone apps, but it could be close. As for the what, the requisite mindset shift means, by definition, that we don’t yet know what those apps will be. There will be surprises.

Mundane Will Win

Going back on the previous statement… though we don’t know the exact nature of AR’s eventual killer apps, there are some attributes we believe they’ll carry. For example, they’ll have some novelty but will rely more on factors like all-day utility and capacity for frequent use.

Pointing to a few examples in today’s landscape, AR experiences that have these traits include “try before you buy,” product visualization. They solve real pain points and align true utility with monetizable and commerce-oriented experiences. The latter is where brands will actually invest.

An even better example can be seen in Google’s interlinked AR efforts. That includes visual search, which has the greatest potential “all-day” use case in terms of utility and frequency. And VPS will solve real user pain points — on city streets and retail environments (monetizable).

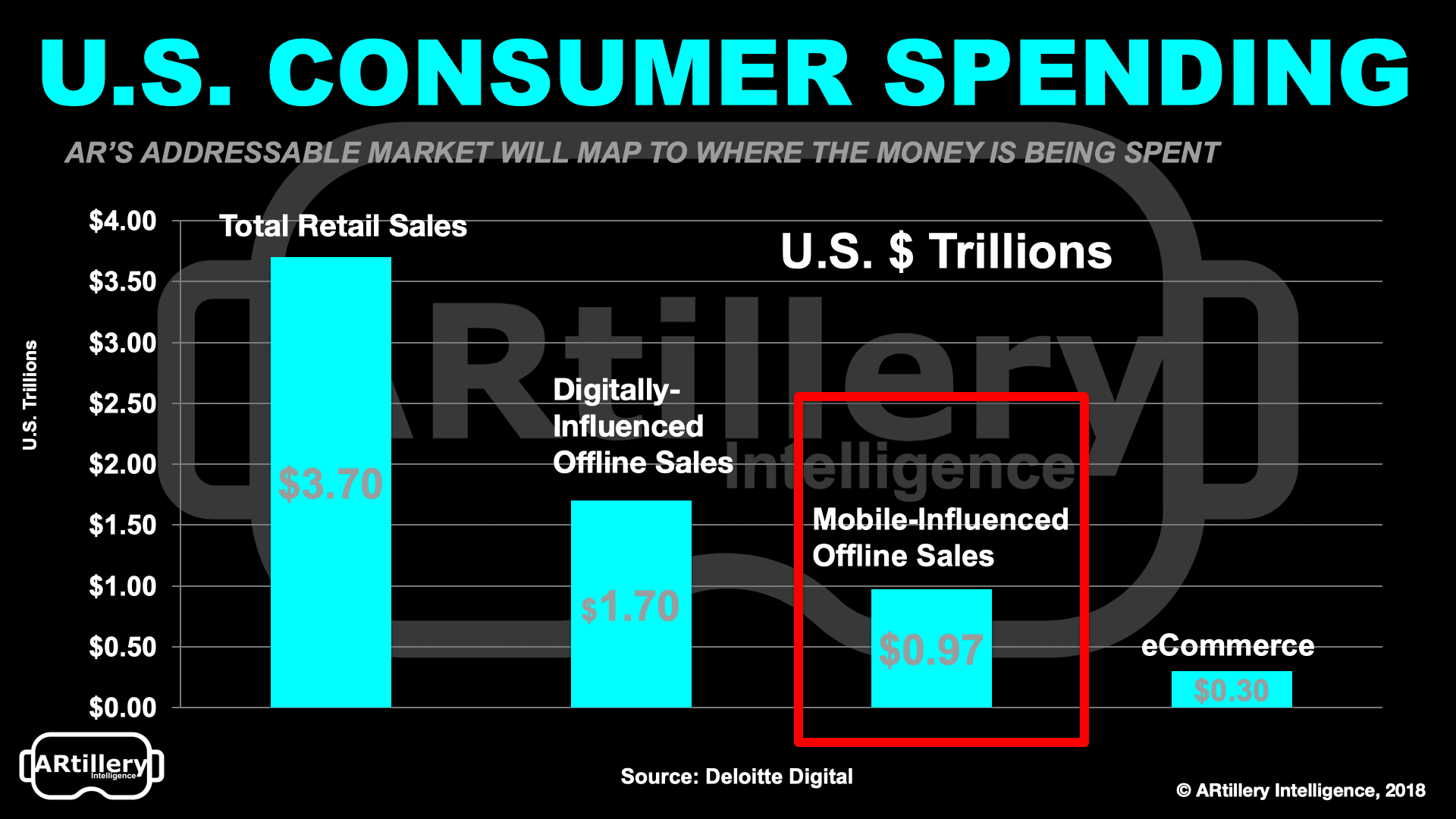

To put some numbers behind that, there’s $3.7 trillion in offline U.S. spending. An increasing portion of that spend — about $1 trillion — is influenced by mobile. This is where AR will live, as it compresses that online-to-offline consumer journey. Google is particularly vested in this vision.

Picks and Shovels

Another key area of opportunity is AR building blocks. It includes enabling technologies that handle the back-end heavy lifting and let developers focus on their front-end UX. Examples are companies like 6D.ai or AR as a service (ARaaS), such as Niantic’s Real World platform.

Another key building block will be creative tools like Adobe Aero, Amazon Sumerian and anything that democratizes AR creation and distribution. This is required to boost the libraries of 3D graphical assets that will populate all of these AR experiences that we envision.

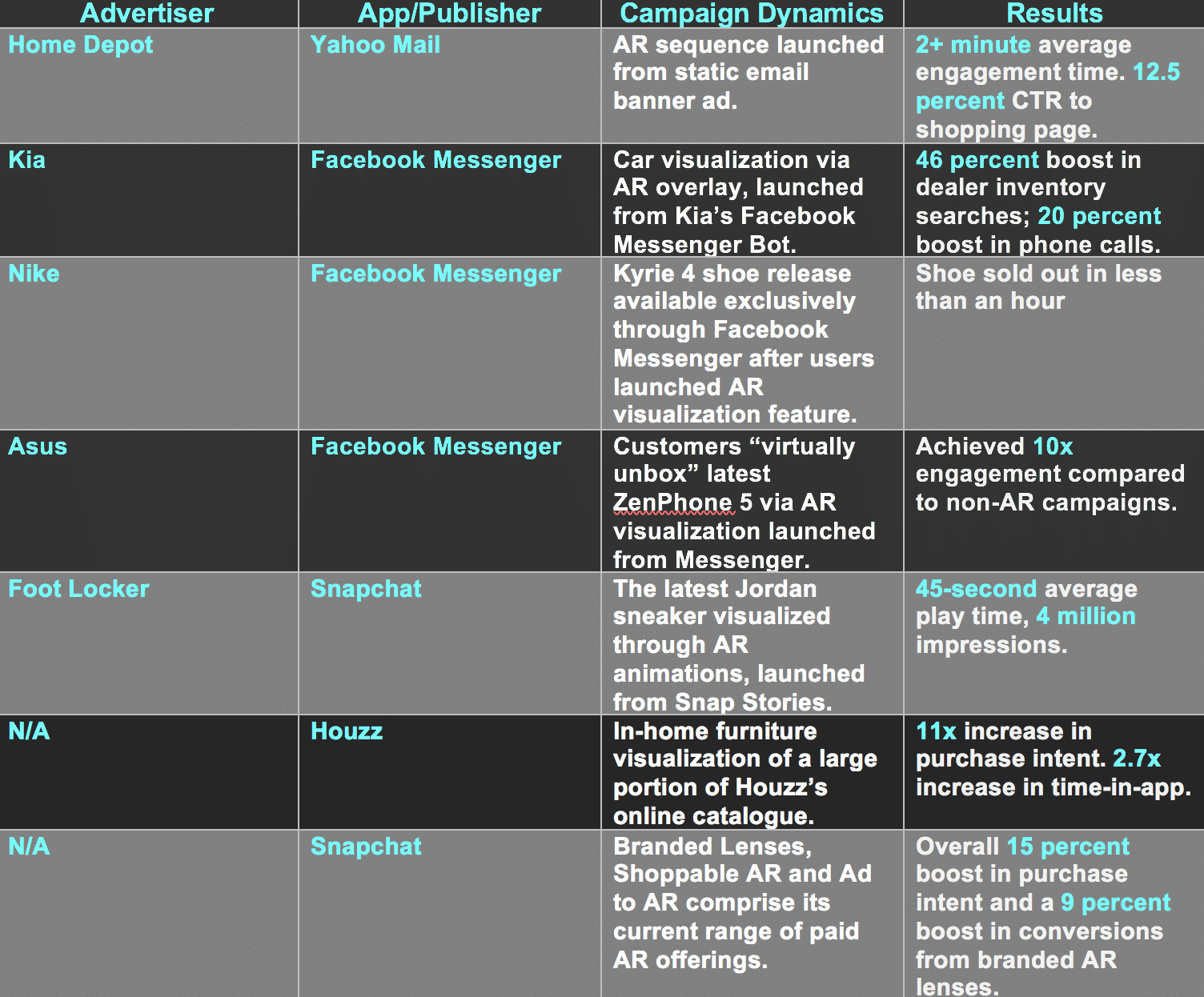

That includes a related opportunity and confidence signal: brand advertising. It’s currently one of the few places being monetized in AR, with just over $400 million spent in 2018. That’s mostly branded AR lenses in Snapchat and Facebook. We project it to grow to $760 million this year.

The appeal to advertisers is strong brand engagement due to immersive use cases like trying on cosmetics. And it’s going beyond brand awareness to drive actual conversions with baked in transactional functionality. This makes it a rare full-funnel ad medium (see chart below).

Business Model Validation

Lastly, one big confidence signal is real revenue generation. Beyond the hundreds of millions in AR ad revenue per the above, there’s already $ billions in in-app purchase revenue. Specifically, Pokemon Go has driven more than $2 billion in revenue to date from in-app purchases (IAP).

To be clear, this revenue isn’t fully attributable to AR, as Pokemon Go is an experience in which AR is just one (growing) component. But it’s still a confidence signal — and not just for the question of whether or not AR revenue exists but how. Lots of signs point to IAP as a go-to model.

Not only is IAP validated in other segments of the mobile gaming world, but it’s fitting to AR’s early stages. As our survey data with Thrive Analytics indicates, AR is too early and unproven to get users to pay upfront for premium apps. More survey data are unpacked in the video below.

Beyond all these consumer AR confidence signals, there are of course negative signals we’ll continue to examine on AR Insider. Meanwhile, see the full presentation below and stay tuned for more recaps from AWE NITE in our XR Talks series.

For deeper XR data and intelligence, join ARtillry PRO and subscribe to the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.