This post is adapted from ARtillery Intelligence’s report, Spatial Computing: 2019 Lessons, 2020 Outlook. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

At this stage of spatial computing’s lifecycle, it’s becoming clear that patience is a virtue. After passing through the boom and bust cycle of 2016 and 2017, the last two years were more about measured optimism in the face of the sobering realities of industry shakeout and retraction.

At the precipice of 2020, that leaves the question of where we are now? Optimism is still present but AR and VR players continue to be tested as high-flying prospects like ODG, Meta and Daqri dissolve. These events are resetting expectations on the timing and scale of revenue outcomes.

But there are also confidence signals. 2019 was more of a “table-setting” year for our spatial future and there’s momentum building. Brand spending on sponsored mobile AR lenses is a bright spot, as is Apple AR glasses rumors. And Oculus Quest is a beacon of hope on the VR side.

Mobile: The Near Term Play

After covering the ‘What, When & Why’ of Apple’s AR play, what about the “here and now” AR Opportunity? AR glasses’ older cousin has reached ubiquity and global scale. We’re talking of course about smartphones, and the less-evolved form of AR that will be a stepping stone.

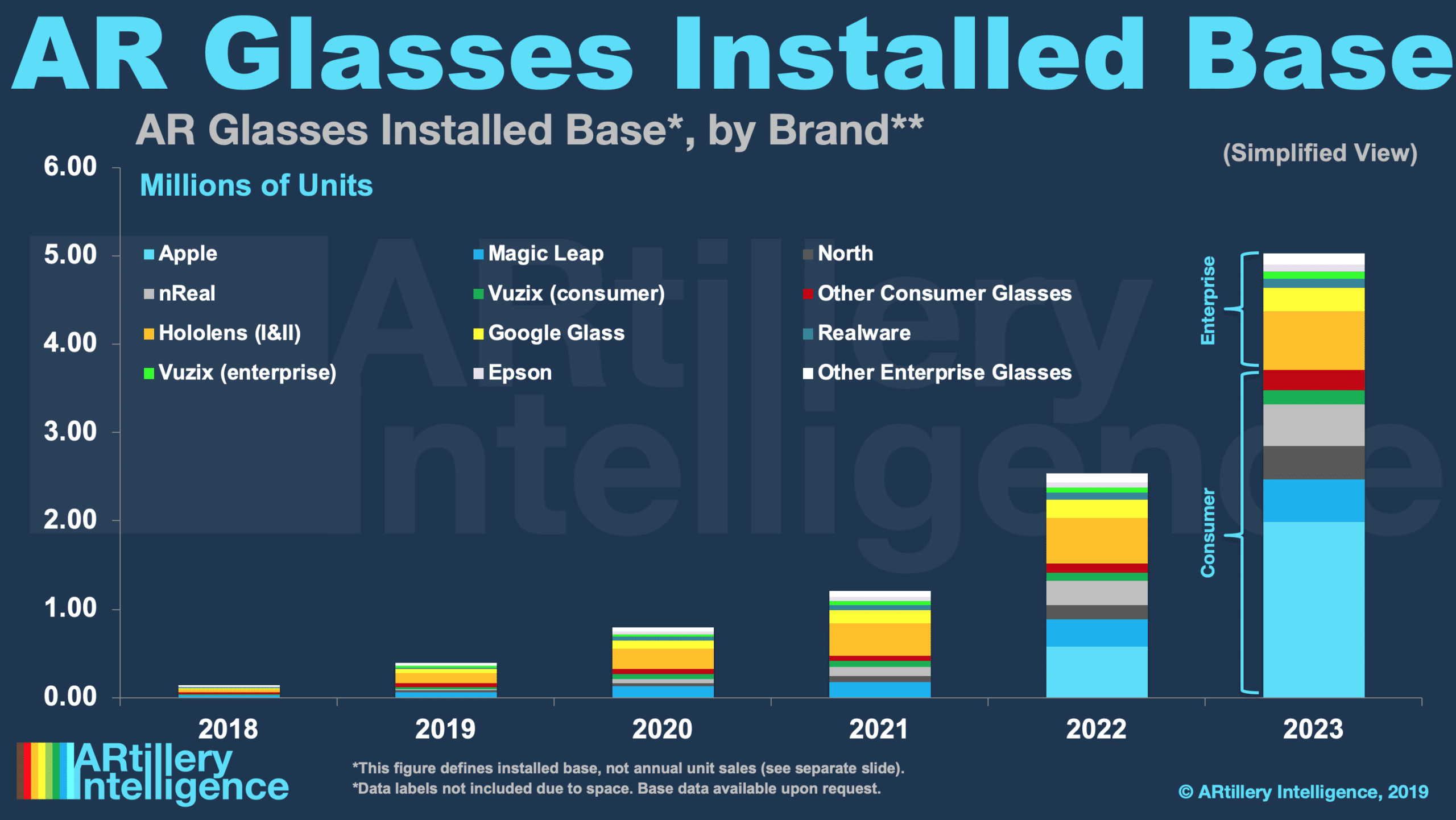

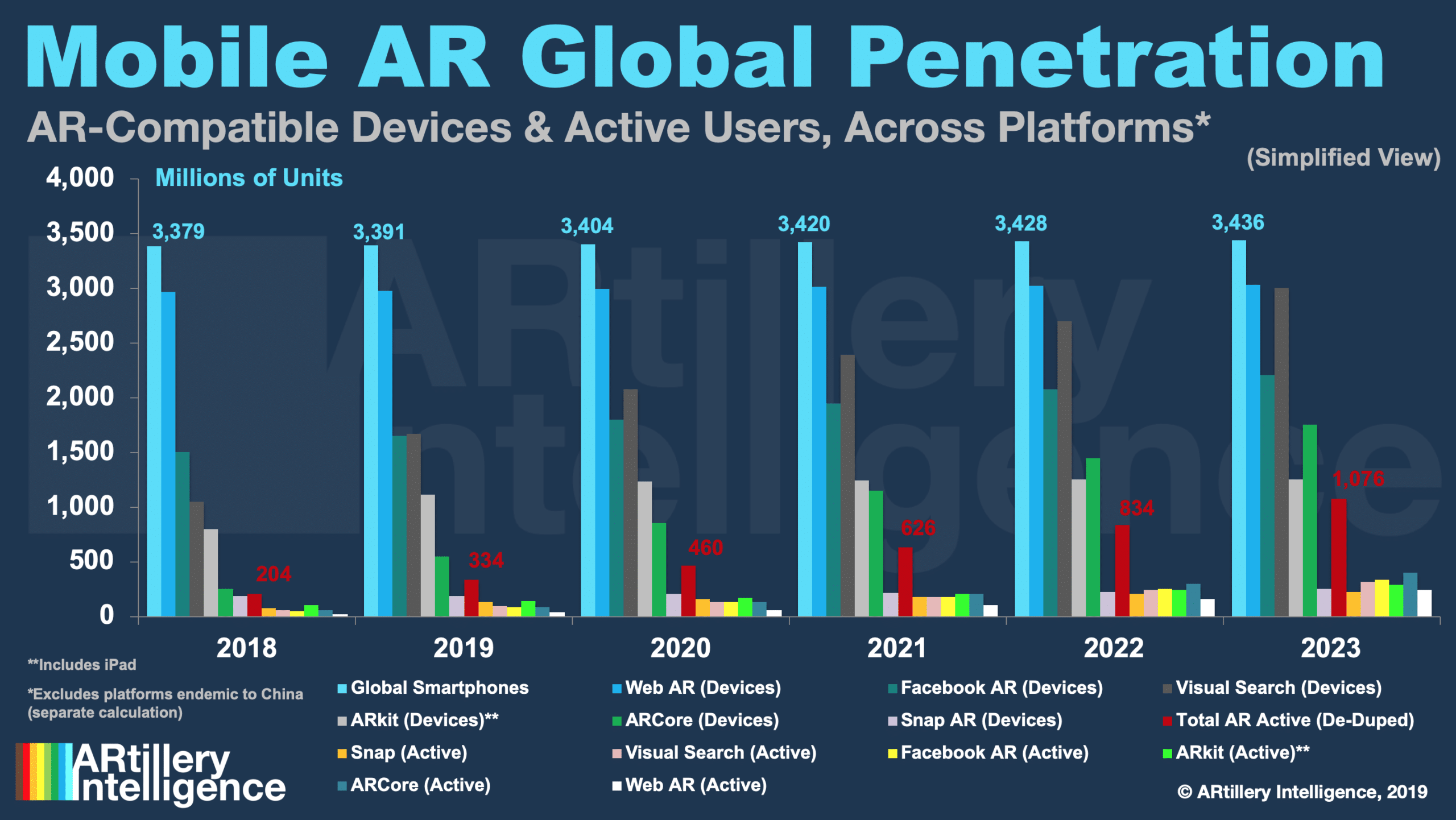

To provide some high-level figures to put in perspective, there are about 3.39 billion global smartphones today, growing to more than 3.4 billion by 2023. That makes the smartphone installed base 700x our 2023 projection for AR glasses’ installed base (5 million in-market units).

This is a sobering realization for smartglasses proponents, but an important one. Even if Apple launches AR glasses and inflects the market in the way we project, smartglasses still have a long road to ubiquity. This is why mobile AR is where the action is today… a numbers game.

Mobile scale has been a rallying cry for the AR industry’s potential reach until AR glasses arrive en masse. However, it’s more relevant to examine mobile AR compatibility and active use, as opposed to the overall universe of global smartphones. The former reflect the addressable market.

334 Million-Strong

The common industry rhetoric at events and in the trade press is that AR’s installed base is “1 billion units.” This is true if counting Apple (ARkit) and Google (ARcore) compatibility. However, an increasingly-fragmented set of mobile AR platforms creates a more complex picture.

According to ARtillery Intelligence’s latest AR revenue forecast, of the 3.39 billion smartphones on the planet, those that are AR-compatible include web AR (2.97 billion), Facebook’s Spark AR (1.6 billion) Snap’s Lens Studio (210 million) and several others represented in the chart below.

But the above figures measure AR compatibility. The number that matters more is active AR users. That total comes to 334 million, growing to 1.076 billion by 2023. This figure tallies and de-duplicates active users across all of these platforms, as there is some overlap between them

To qualify, this doesn’t include platforms endemic to China. These are significant, but their sizing is done separately in terms of addressable market analysis. That’s because users of these platforms aren’t always addressable to companies outside of China, so it skews the strategic implications.

Confidence Signals

Though the above figures are strong, Mobile AR is more of a layover than a destination. Mobile AR doesn’t live up to AR’s true promise, but is warming the world up for it. That goes for consumers as well as developers, who must condition their thinking for natively building immersive experiences.

This involves several formats taking shape as developers and tech companies feel out consumer demand. The two forms of AR that have gained the most traction are object visualization (placing objects in your space) or selfie lenses to dress up one’s appearance. These span a range of uses.

The former involves rear-facing camera AR to augment the world, while the latter involves front-facing camera AR to augment people. As Snap’s Carolina Arguelles said at AWE Europe, AR content has to be relevant… and there’s nothing more relevant to people than their own faces.

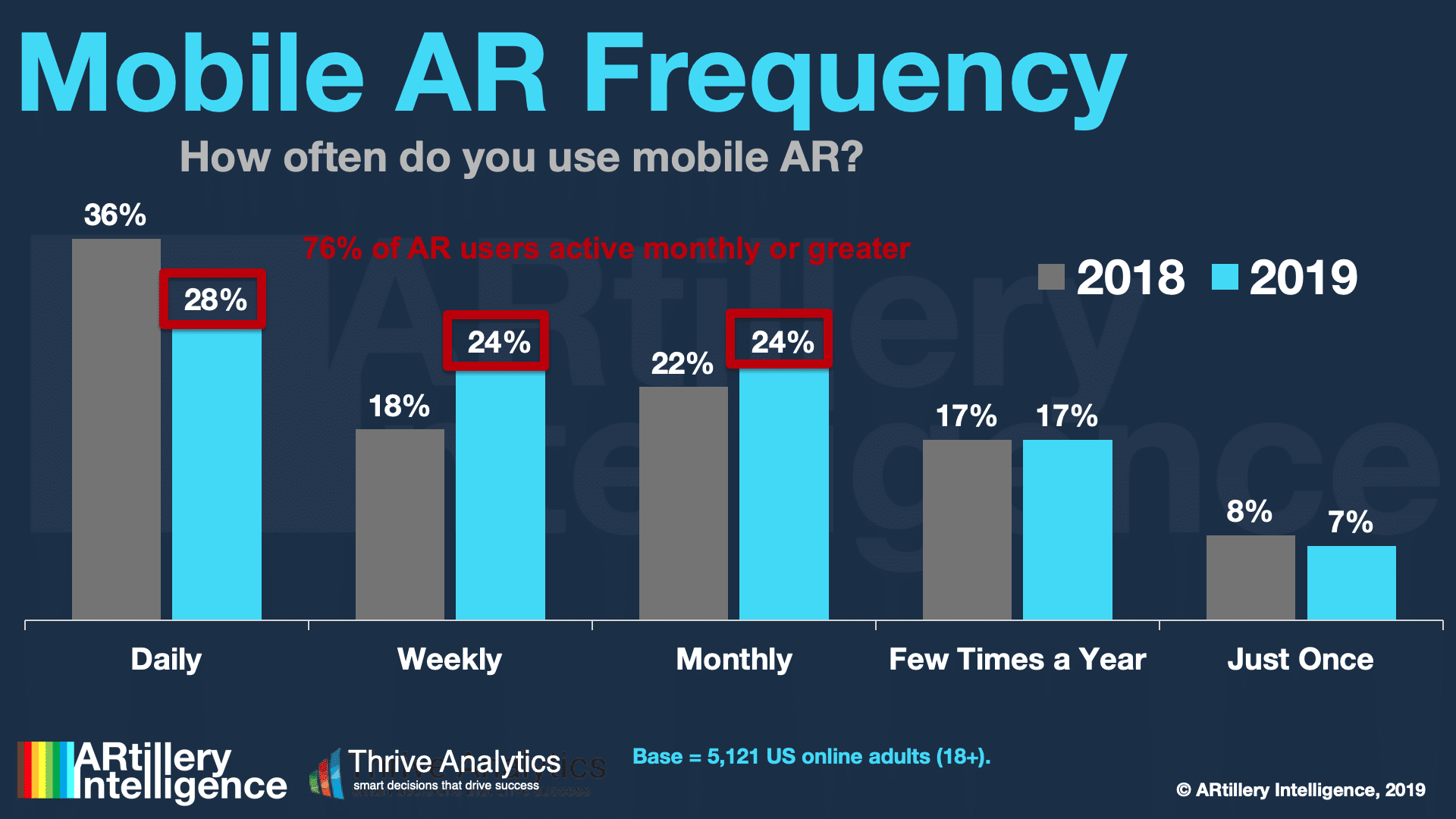

This principle has driven lots of high frequency and deep engagement for lenses. ARtillery’s consumer AR survey with Thrive Analytics shows that 67 percent of AR users reported monthly or greater frequency and 78 percent reported high satisfaction. Snap also reports 30x daily use.

Revenue Mix

Facebook meanwhile served one billion AR lens engagements in the year prior to May 2019 across News Feed, Portal and Messenger. The biggest sleeping giant could be Instagram, which just launched AR. It could be a winning formula with Instagram’s camera-forward users.

Snap has shown even more scale with 15 billion AR lens engagements, 163 million daily AR lens users and 500,000 total lenses created. The ad dollars are following, given strong performance for immersive product try-ons for branded AR lenses. Brands are seeing results and doubling down.

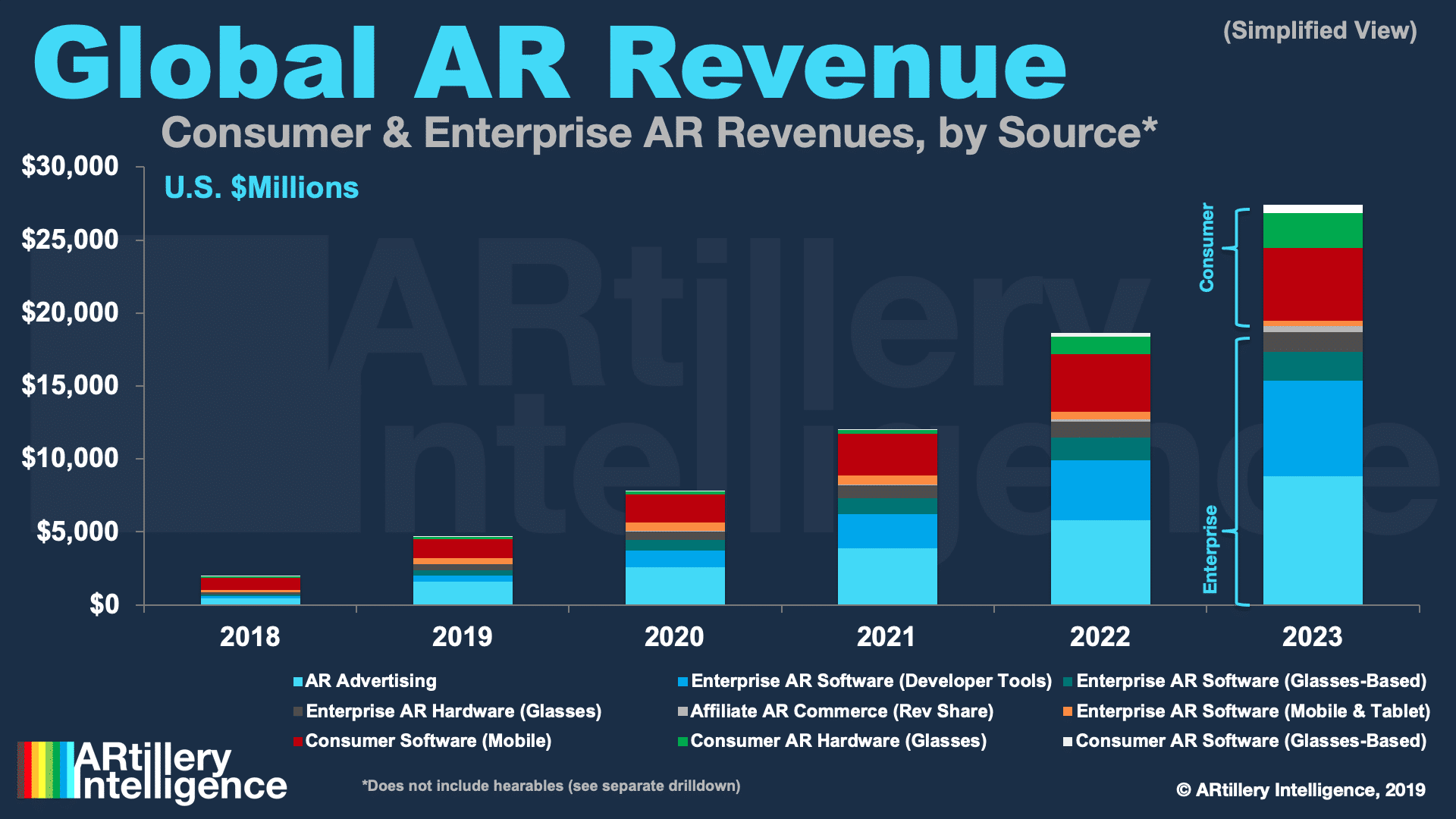

Specifically, ARtillery Intelligence projects AR ad revenue to grow from $1.58 billion last year to $8.8 billion by 2023. That consists mostly of brand-sponsored AR lenses in the above channels but will grow into other channels like messaging and formats like high-intent visual search.

This is the biggest revenue source in AR, followed by in-app-purchases, mostly from Pokémon Go, and AR as a Service (developer tools) as we examined in a recent report. This revenue mix will evolve over the coming years as mobile AR user experiences and expectations likewise evolve.

Check out the full report here.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.

Header Image Credit: Apple