This post is adapted from ARtillry Intelligence’s latest report, XR 2018 Lessons, 2019 Outlook. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

2018 was a reflective year for XR. After an exuberant 2016, followed by a corrective 2017, XR industries settled into a moderate pace. This includes reset expectations on the size and timing of AR & VR markets, as well as acceptance that aspirations will take longer to materialize.

But we saw deep-pocketed tech giants charge ahead with XR. With strong contention that XR represents the next computing shift, they’re investing in the future of their platforms by gaining early market share and technological edge. And they’re each attacking XR from different angles.

Apple is investing in AR to fertilize the ground for its future hardware: AR glasses. Google is cultivating visual search, a close cousin of AR, as a search modality. Amazon is embracing AR to boost e-commerce, and Facebook is spending billions to position a VR powerhouse.

Despite XR market softness, it was these moves from tech giants that provided confidence in 2018 for the eventual market arrival. Indeed, there’s no bigger vote of confidence in a technology and a market than billions of dollars in long-term bets. We believe this will continue into 2019.

One of those investments will be Facebook’s continued subsidization of VR headsets, through aggressive pricing. It’s executing a classic loss-leader approach to gain early market share and build up the installed base of Oculus headsets. This is already accelerating consumer adoption.

We also learned important lessons in 2018 about AR adoption and behavior. Mobile AR, despite its potential scale, is gated by consumer AR interest and app quality. And these factors need more time in the oven. The quality of many ARkit apps hasn’t sold the masses on AR just yet.

But though the scale is relatively low, mobile AR users are showing strong engagement in terms of frequency and other behavior. In formats where engagement is measured heavily, such as AR ads (branded AR lenses), performance indicators and advertiser ROI are already quite strong.

Meanwhile, there were wild cards played in 2018. Magic Leap One finally launched, coupled with even more ambitious promises. Apple’s acquisition spree and patent filings point to its AR glasses circa 2021. And the AR Cloud’s importance emerged into the collective consciousness.

So the question is, where are we now with these and other XR sub-sectors? And what can we expect in 2019? We tackle those questions in the latest report and will unpack some of the findings here over the coming weeks. For now, here’s a quick taste of our 2019 predictions.

1. Mobile AR Promising, But Slow

Mobile AR continues to hold the promise of scale, due to almost one billion ARkit and ARCore-compatible (and several more webAR-compatible) smartphones globally. But the more relevant figure is active users, which is much less: 129 million. The medium needs more time to develop, including underlying technology, developers’ native footing, and user acclimation – all of which go together.

2019 Prediction: Consumer AR revenue will reach $3.3 billion in 2019, $2.9 billion of which is in-app-purchases. The first killer app for world-immersive and SLAM-based AR could be released as early as late 2019. This will be two years after the June 2017 launch of ARkit – the same timeframe after the iPhone 1 when killer apps emerged (Uber, Waze, Foursquare, etc). Killer app(s) will likely be communications, social or a utility AR experience.

2. AR Cloud is the Lynchpin.

The AR cloud came into the collective consciousness in 2018, after it was apparent that AR apps don’t work the way most people expected. The need for multi-player support, persistence and other functions invoked lots of discussion around the AR cloud as the missing puzzle piece. In response, several AR cloud startups launched and tech giants formed AR cloud strategies.

2019 Prediction: The breakout category in 2019 won’t just be the AR cloud but the broader world of XR enabling-technologies or “building blocks.” That includes tools that streamline or democratize XR creation and distribution, such as AR as a Service. Graphical assets will be a currency in AR commerce and advertising, so their creation tools (Amazon Sumerian, Adobe Aero) will likewise grow in value.

3: AR Ads Already Working

Among the XR revenue categories projected over the coming years, one that’s already bearing fruit is AR advertising. According to ARtillry Intelligence’s latest forecast, the sector made $418 million in revenue in 2018. This has manifested mostly through branded AR lenses from social apps like Snapchat and Facebook.

2019 Prediction: AR advertising will reach $761 million in 2019, and we project it to grow to $2.4 billion by 2022. This will continue to be dominated by display advertising (social lenses) in the coming year. Visual search, a la Google Lens, will gain ground on display in later years as its complexity will cause it to bloom late. But it’s high-intent use case, just like search, will be a strong revenue driver in a few years.

4. Enterprise AR: The Sleeping Giant

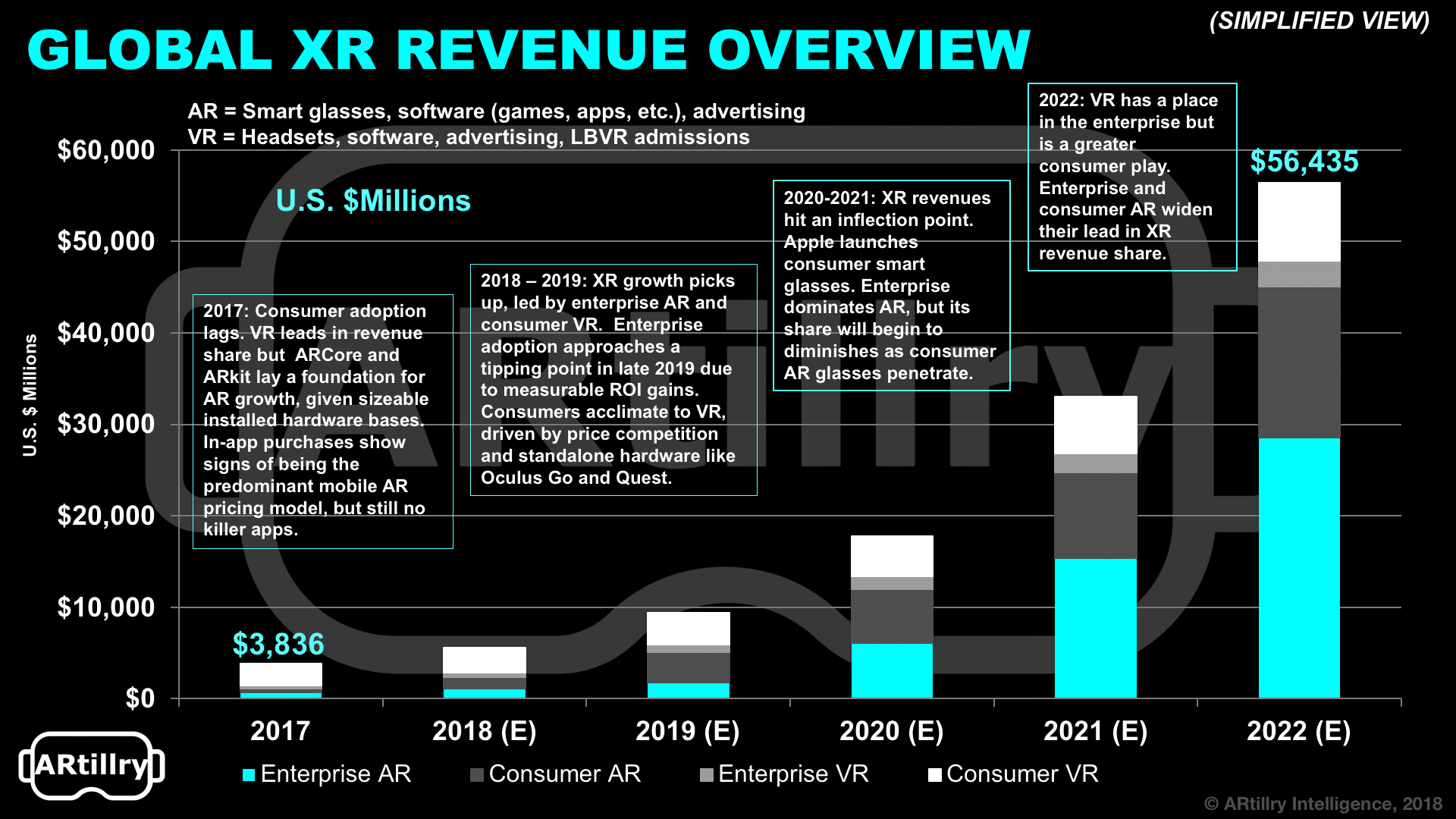

Enterprise AR is the largest XR sub-sector in the outer years of ARtillry Intelligence’s global revenue forecast, reaching $28.5 billion. That will mostly be driven by demonstrable ROI in areas like industrial productivity. But despite that continually-validated ROI story, there’s still meaningful enterprise inertia and risk aversion.

2019 Prediction: Enterprise AR inertia will continue into 2019, and be slowly eroded by its momentum and continued ROI proof in vendor case studies. The sector will reach an inflection point, after which adoption accelerates… but that won’t be in 2019. Likely happening in mid-2020, it will follow the pattern of adoption we saw with enterprise smartphone adoption over the past decade.

5. Consumer VR Promising But Still Soft

Though it leads all XR sub-sectors in revenue today – driven by gaming – VR revenues are beginning to be outpaced by other XR sub-sectors. This is mostly due to flattening revenue from early adopters who themselves plateaued in volume. With that realization, price competition took over the sector in 2018 in order to penetrate further into mainstream consumer segments.

2019 Prediction: We’ll continue to see aggressive price competition from Oculus, which will cause more contraction in the consumer VR segment. Oculus Go and Quest will pull ahead in 2019 and increase their lead of headset (unit) market share. Oculus Go in particular will reach 2019 sales of 1.8 million, while Quest, launching mid-year, will reach a quarter of a million in unit sales.

For more detailed narrative and data graphics, see ARtillry Intelligence’s latest report, XR 2018 Lessons, 2019 Outlook.

For deeper XR data and intelligence, join ARtillry PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.