AR has seen its ups and downs. The excitement and expectations that consumed 2016 and 2017 were followed by a bad hangover in 2018 and 2019. So where does that leave us now and, more importantly, where are we headed next?

Whenever this question arises, the go-to explanation is AR’s period of repentance in the “trough of disillusionment,” of Gartner’s Hype Cycle. This is a perfectly valid construct but it’s arguably overused as fodder in nearly every conference presentation these days on AR’s status.

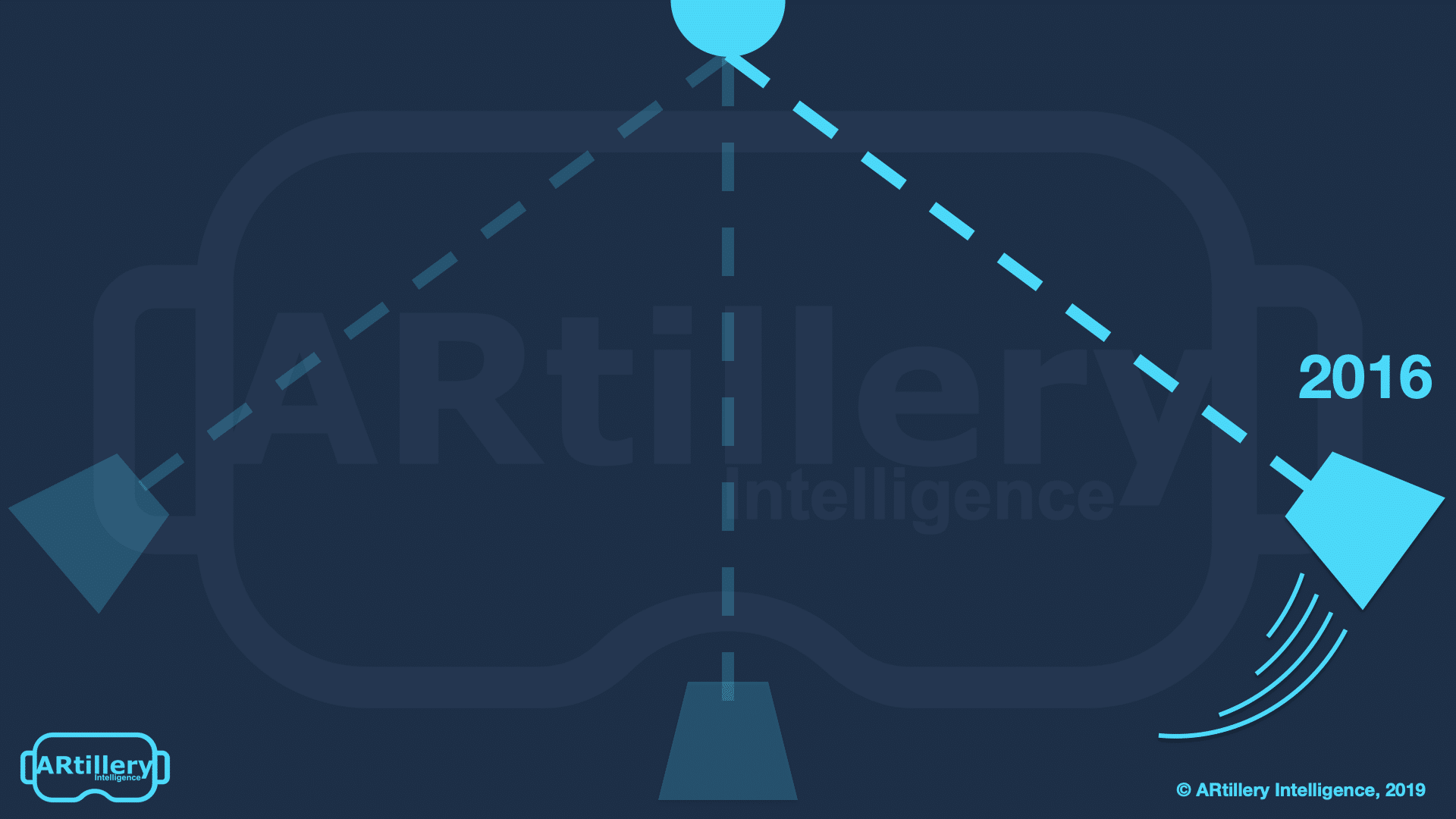

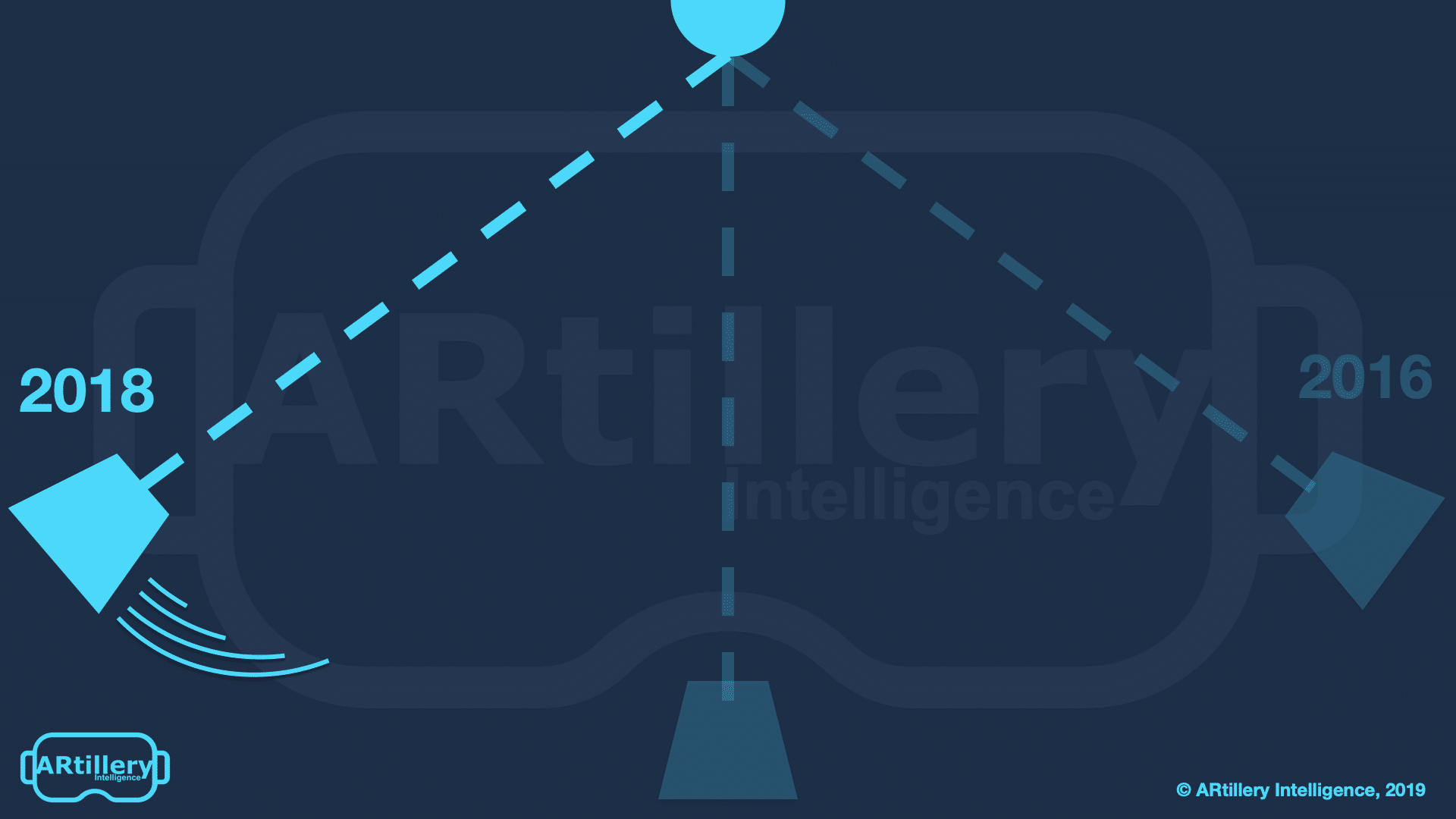

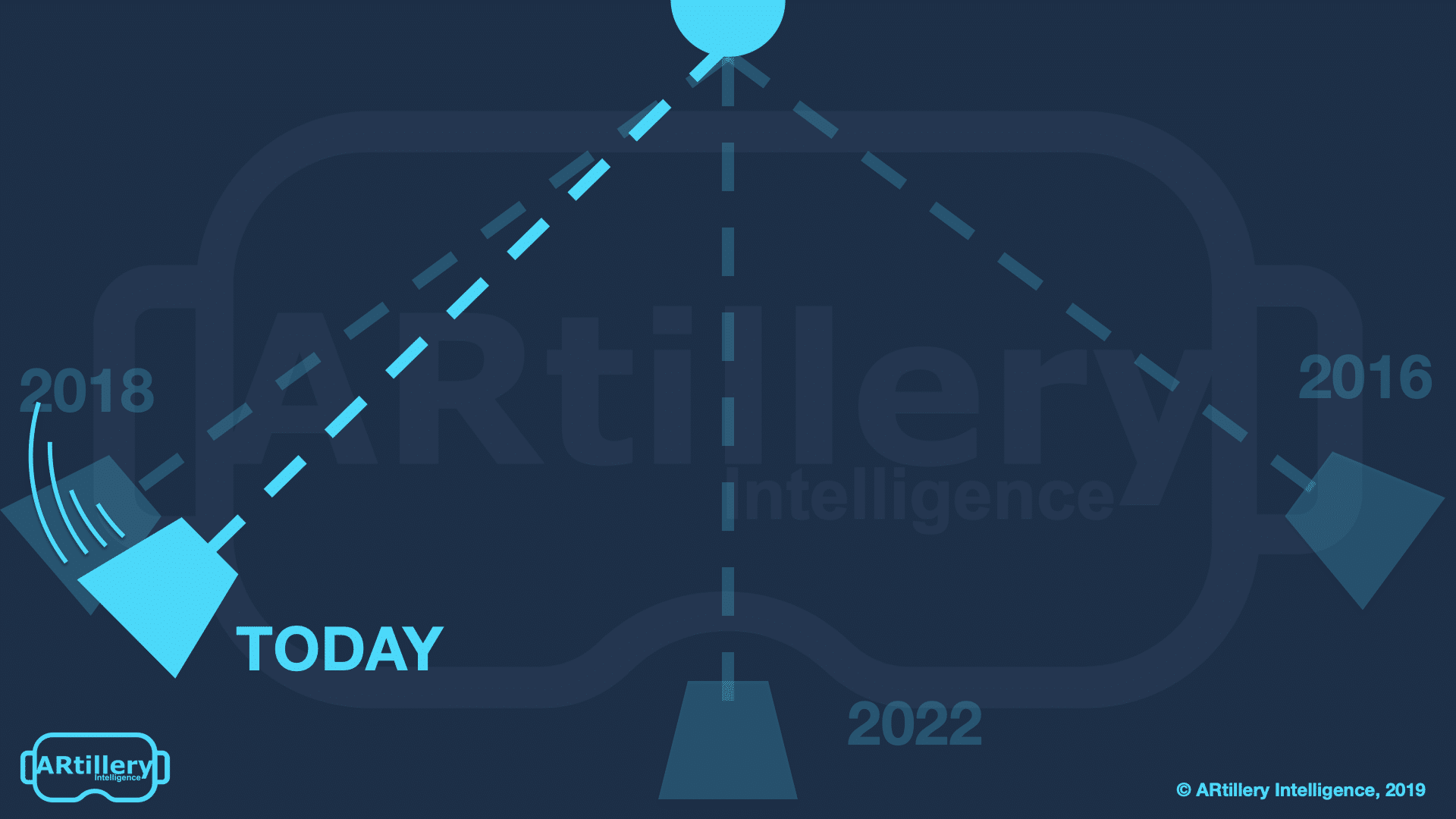

So we’ve begun to think about AR’s lifecycle using a different construct: that of a pendulum. Often in early stage sectors, a pendulum metaphorically swings in one direction that represents overblown expectations, supply-side saturation and lots of venture funding (arguably too much).

Then, it swings in the other direction as a bit of a backlash to the overabundance. That period is defined by sobering realizations that the technology isn’t ready, or that it’s not gaining the traction previously expected. A shakeout ensues as companies fail to secure additional rounds of funding.

2002, A Spatial Analogy

But once the worst of that backswing has passed, things move towards a happy medium. Markets then progress at a healthy pace, while supply and demand grow in step with each other. Just like gravity compels the pendulum to the center, market forces compel supply/demand equilibrium.

What follows is a more measured and realistic period of market growth. The previous hockey-stick growth charts give way to slower, but more reliable, industry revenue projections. Our research arm ARtillery Intelligence releases its AR forecast this week and this thinking is represented.

A historical example is the 2000’s dot-com bubble. We saw overblown expectations, followed by a backlash/recessionary period. But then around 2002, things moved slowly towards measured progress, and the rise of tech giants like Google, Facebook, and the web 2.0 movement.

So that goes back to the question of where we are now with AR. Though the extent of the pendulum swing in either direction might be smaller, we believe AR is in that 2002 sweet spot where the worst is behind us, and we’re moving (slowly) towards healthy growth and equilibrium.

What makes us say that? There are lots of signals that AR’s 2018-2019 hangover has hit its high point, and that the sector is beginning to recover. There’s still a ways to go, but we’re starting to see meaningful traction and scale in mobile AR active use (not just AR-compatible phones).

Mounting Evidence

So what are those signals? At a high level, the biggest confidence signal is money. Tech giants’ investments in AR signals a level of self-serving motivation that will accelerate the technology, and move markets to some degree. Apple, Google, Facebook and Microsoft are all on that list.

But that’s more of a conceptual signal, and is one we’ve covered already — including a report, a chapter in Charlie Fink’s book and a presentation at AWE last month. What about more recent and tangible market signals that AR traction and revenue generation are moving in the right direction?

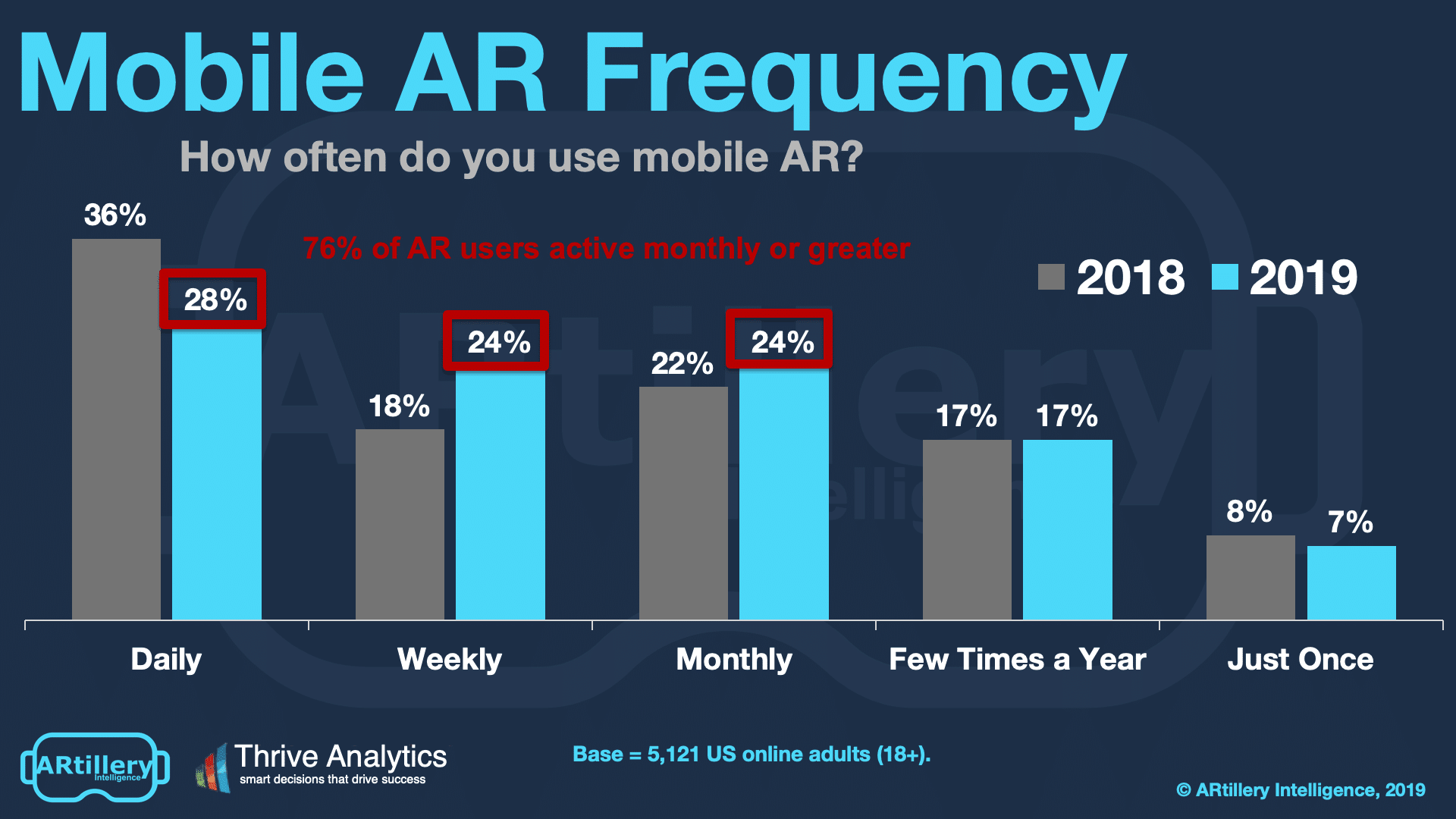

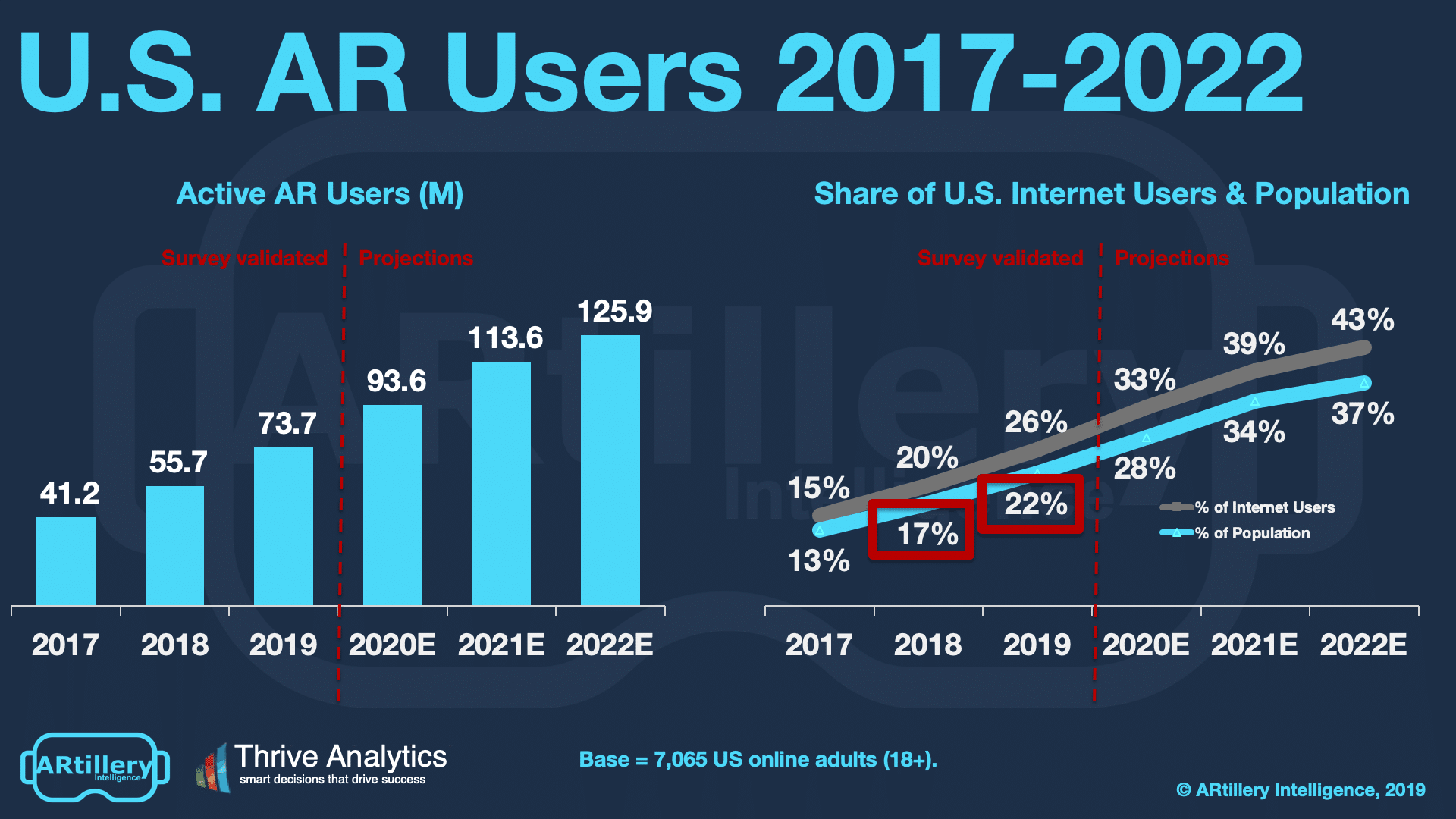

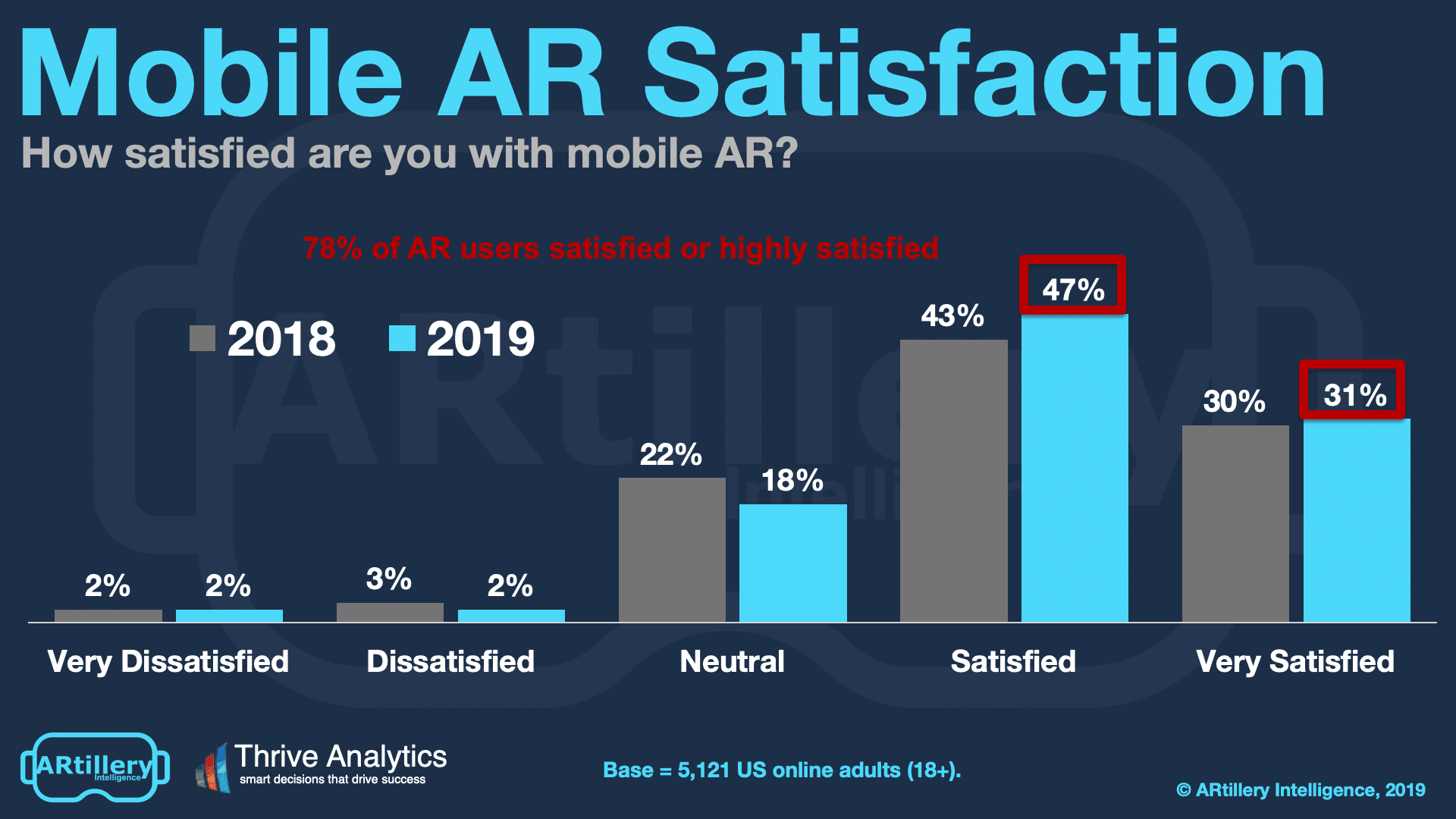

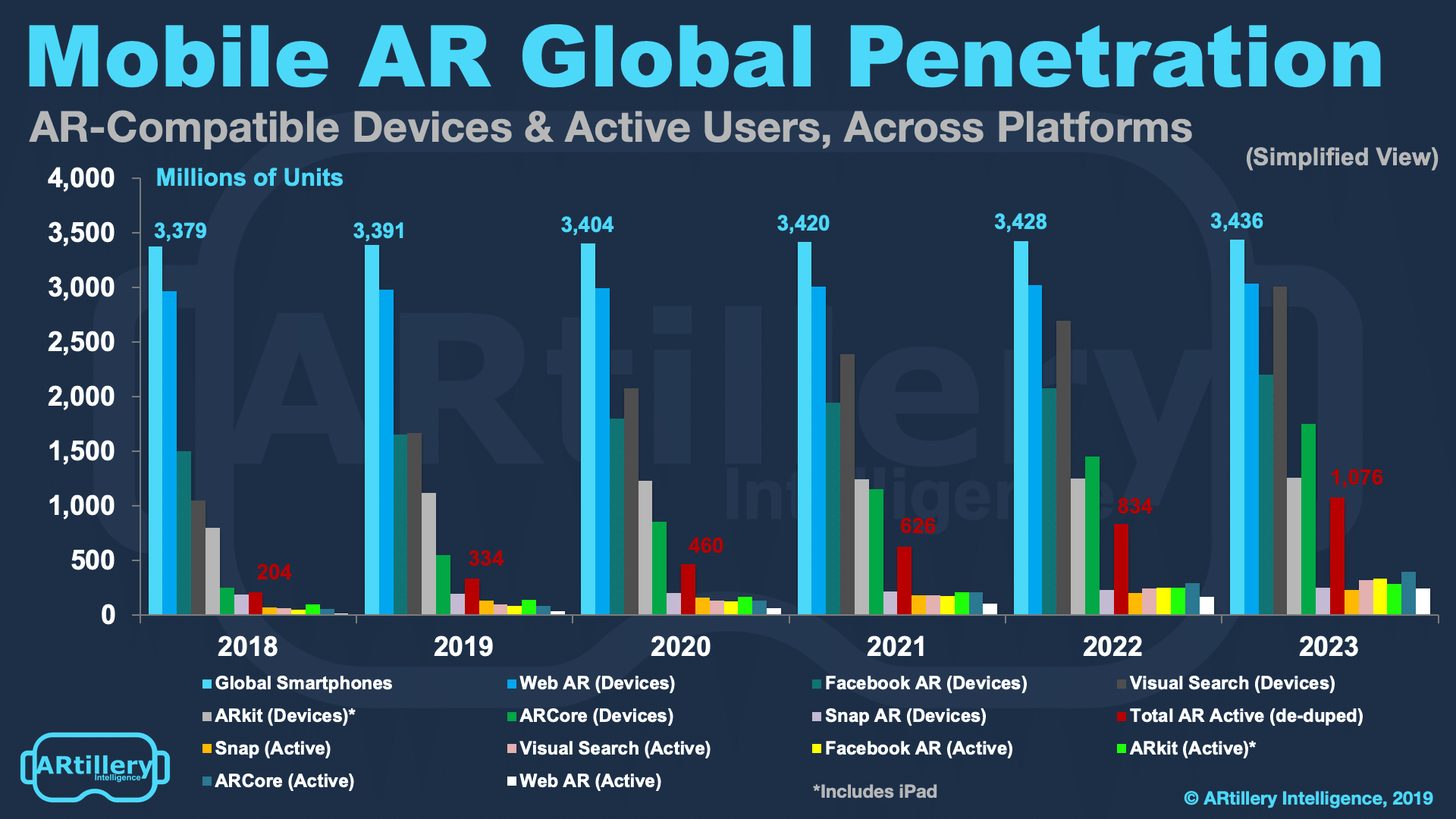

For one, consumer AR usage shows strong signs. In our consumer AR survey with Thrive Analytics, 67 percent of users reported monthly or greater frequency and 78 percent reported high or very high satisfaction. AR active users now total 334 million, up from 204 million last year.

Facebook meanwhile announced at F8 that it served a billion AR lens engagements over the past year across News Feed, Portal and Messenger. The biggest sleeping giant could be Instagram, where it’s just now flipping the AR switch by opening the Spark AR beta “this summer.”

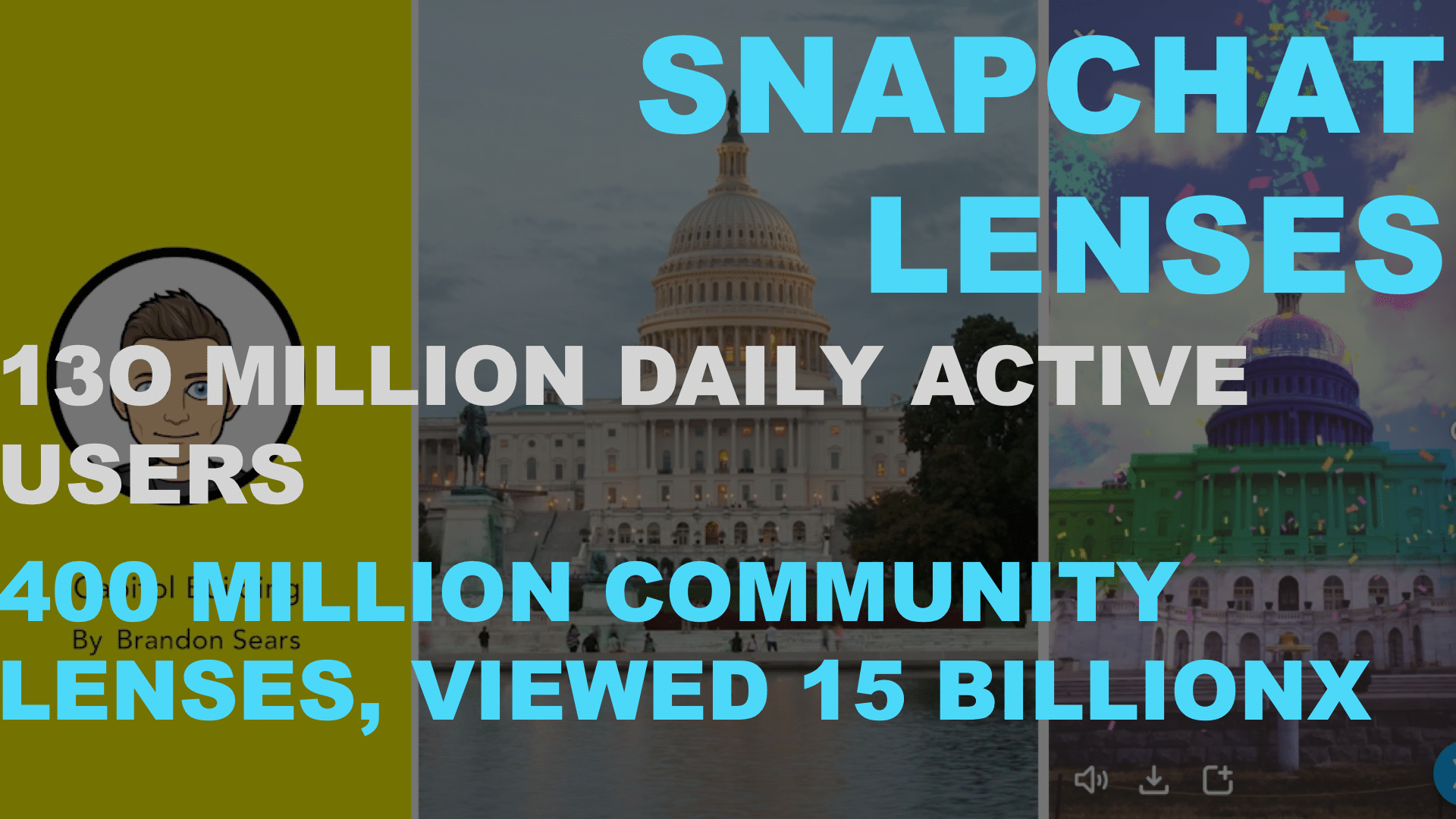

Snapchat has shown even more scale with 15 billion AR lens engagements over the past year, and 130 million daily AR lens users — twice that of last year by our count. And the ad dollars are following, given strong performance for immersive product try-ons with branded AR lenses.

Organizational Layer

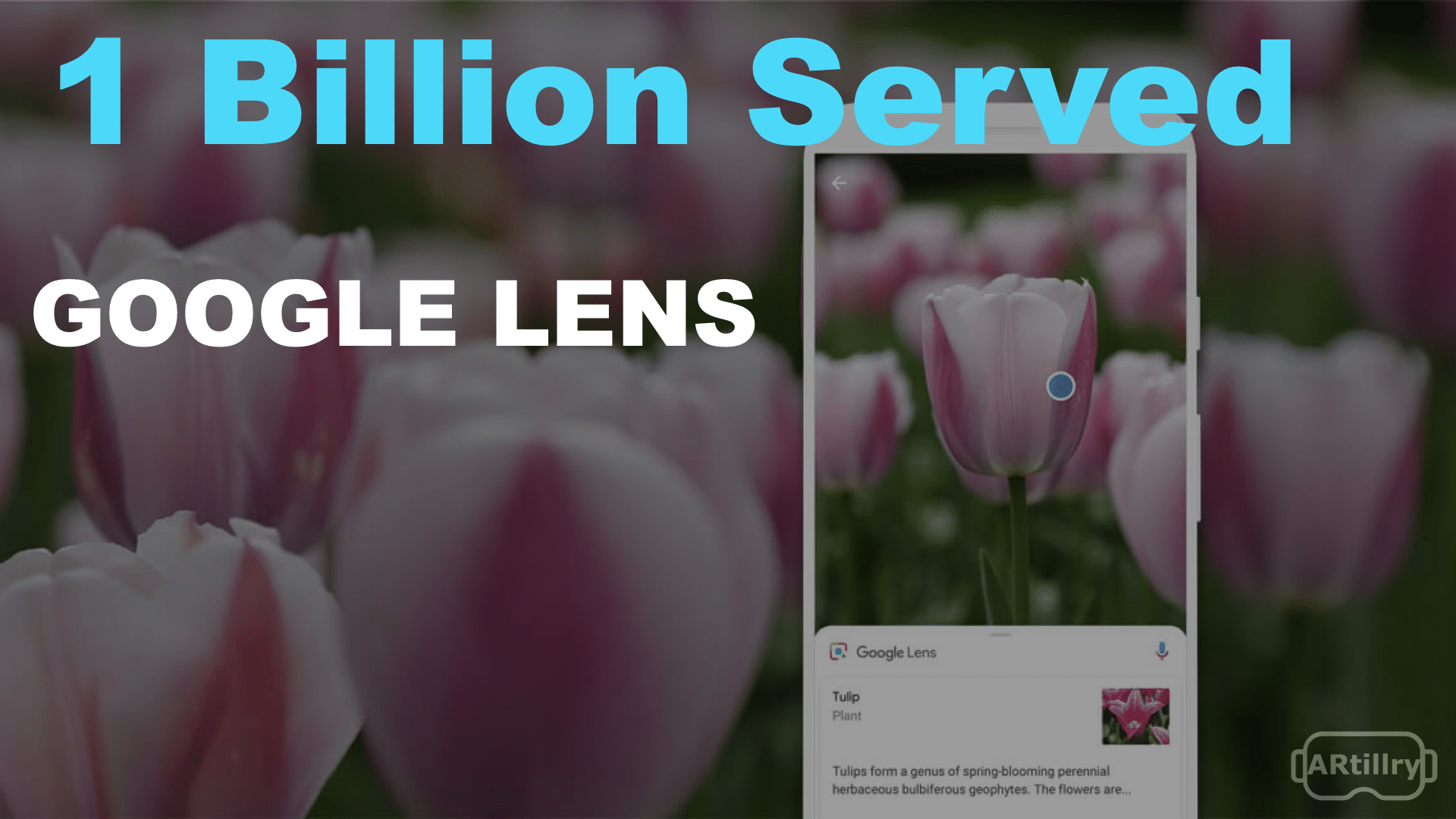

Speaking of Facebook’s billion lens engagements, Google has matched that figure in visual search activations for Google Lens. It also announced that Lens is capable of identifying one billion real-world objects, which will continue to grow to the extent of its visual database.

In fact, Google’s momentum with visual search could be the biggest confidence signal yet for AR. Not only does “following the money” provide confidence per the above point, but Google is showing tangible signs of accelerating AR, such as the integrations and announcements at I/O.

Visual search a la Google Lens is also our top pick for potential AR killer apps. As the technology is refined further and as Google continues to position it in the mobile search flow, it could grow into a high-frequency AR utility. And monetization will follow Google’s established search playbook.

Back to the pendulum, Google started creating immense value during the early-2000’s backswing. It did so with the web’s organizational layer: the search index. That’s where we are now with AR: pre-Google Index. Could the AR cloud be that organizational layer… and that inflection point?

We’ll be watching closely and reporting back daily. Meanwhile, our research arm ARtillery Intelligence releases its bi-annual AR revenue forecast this week, which will put some numbers behind much of the above. You can also check out our recent presentation on this topic below.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.