2020 was a turbulent year for the world, but activity in spatial computing was relatively calm. And that’s actually a good thing as the sector’s early and erratic days have transitioned to slow & steady growth. These are marks of an industry that’s moving into adolescence,

With that backdrop, we embarked on our annual exercise of examining lessons from the past 12 months and projecting the next 12. The result is the report, Spatial Computing: 2020 Lessons, 2021 Outlook, and the latest episode of ARtillery Briefs (video and takeaways below).

The Spatial Spectrum

To level set on definitions, the focal range here is the full spatial spectrum. That includes AR, VR, and all of their subsegments. Those subdivisions include hardware and software, as well as consumer and enterprise use cases. These are each governed by different market factors.

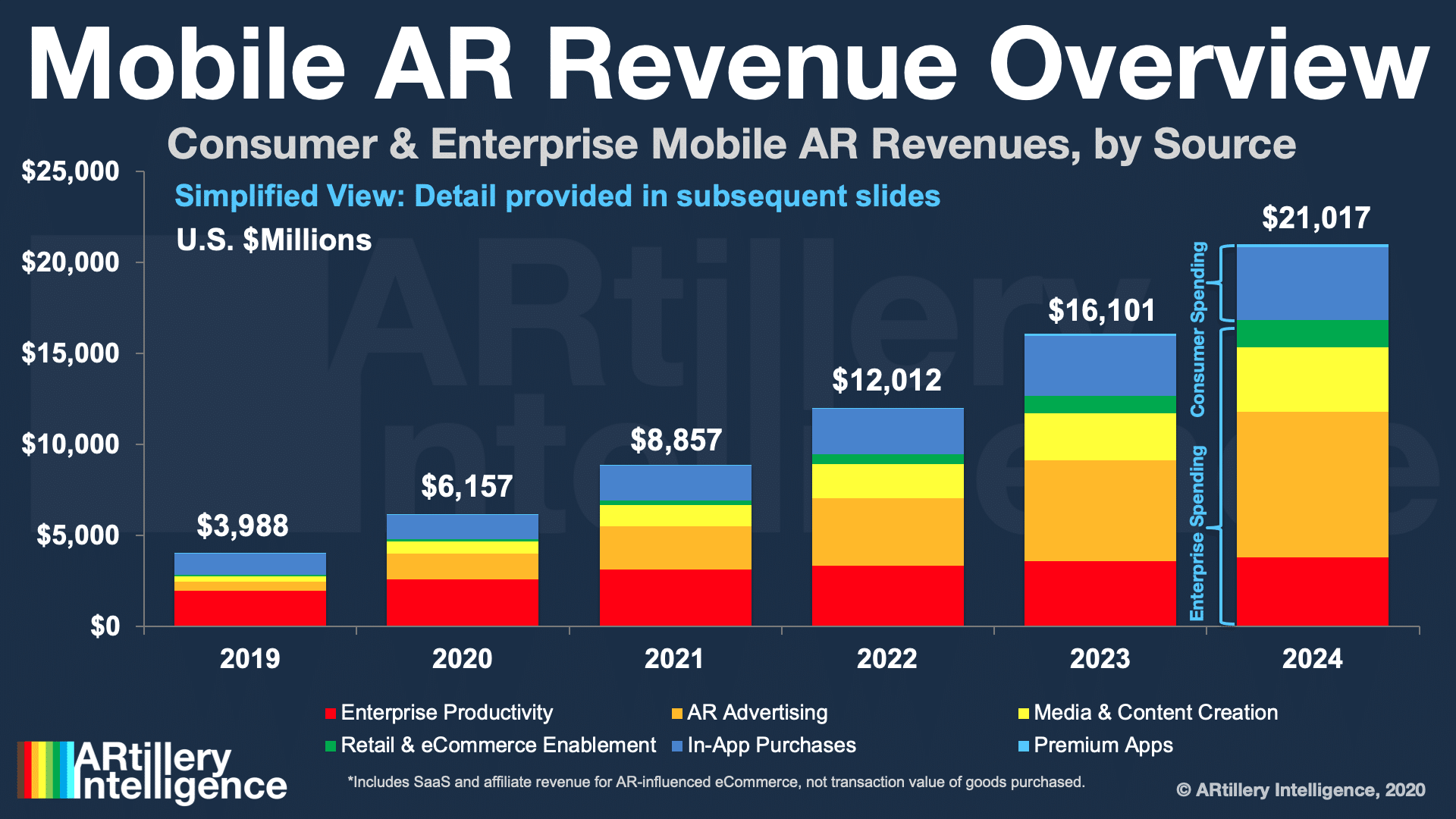

To break that down, one bright spot for AR continues to be smartphone-based, given device penetration. There are 3.46 billion global smartphones, about 3 billion of which are AR-ready and 598 million are AR active. And the underlying hardware continues to evolve, such as LiDAR.

Meanwhile, leading mobile AR business models are in-app-purchases in mobile gaming, and advertising. We estimated the latter to reach $1.4 billion in spending in 2020, driven by continued traction for socially-driven AR lenses, and performance for sponsored lens campaigns.

But Mobile AR’s most significant area of development could be the AR cloud. This involves capturing spatial maps that serve as scaffolding for next-generation AR experiences. Tech giants each have their own spin on AR clouds, which means several potential outcomes.

Lighter AR

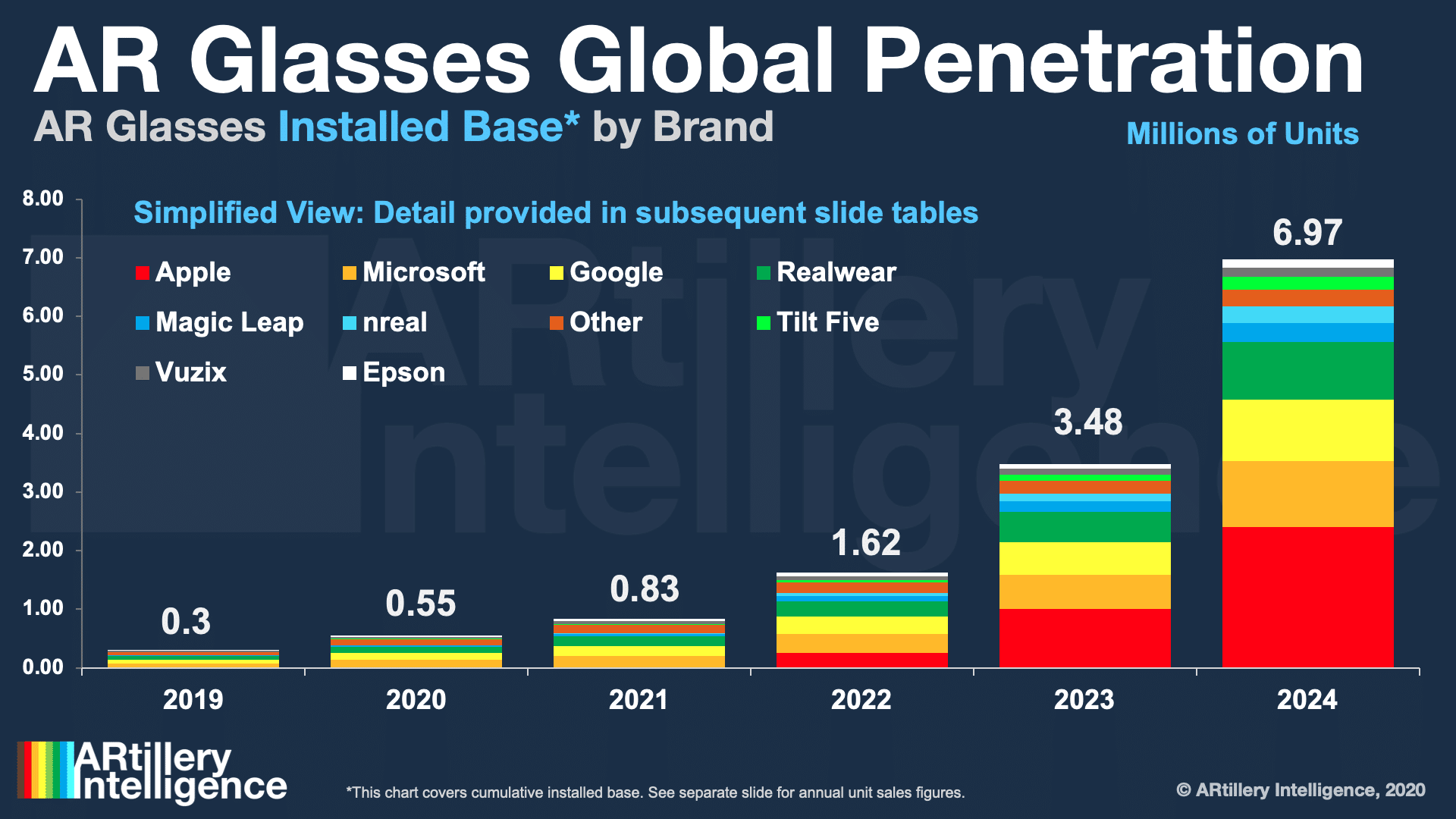

Another device class paving the way for AR is wearables. Just as mobile AR conditions users for spatial experiences, wearables acclimate them to body-worn sensors. And the stakes are high as Apple doubles down on wearables to offset declines from a maturing smartphone market.

Speaking of Apple, AR glasses themselves aren’t ready for mainstream acceptance and won’t gain significant ground in 2021 in consumer markets. But 2022 could be the year when Apple’s AR glasses could arrive and potentially inflect the market, as Apple tends to do.

And if we know Apple, it will prioritize style over graphical intensity and could re-define augmentation through “lighter” forms of AR. That could include things like iOS notifications, “filters” for enhanced vision, or point-of-sale interactions in tandem with Apple Pay.

The best way to think about that is that Apple’s size imposes a fiduciary drive to only shoot for massive markets. And something along the lines of smart sunglasses lets it tap into the multi-billion dollar eyewear market rather than the still-niche consumer AR space.

Steady Gains

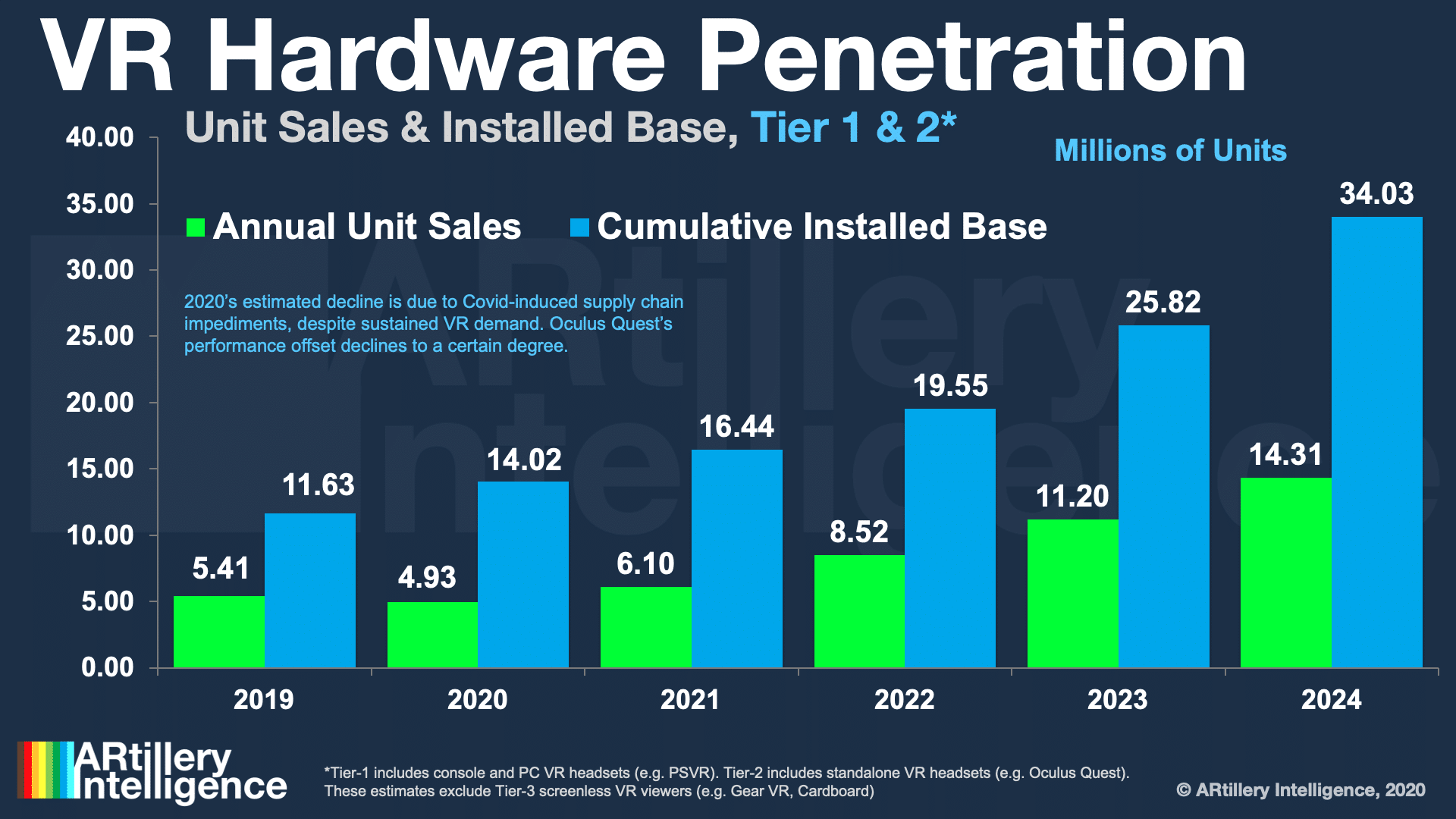

What about VR? It will likewise make steady gains in 2021. That will continue to be propelled by Facebook’s investments in content and hardware, most notably Oculus Quest 2. The device is a hit in every respect with a compelling feature set and mainstream-friendly pricing.

We’re bullish not only on the demand but the supply, as Facebook has beefed up its supply chain, and is meeting orders for Quest 2 more effectively than last year at this time. It learned its lesson in under-anticipating Quest 1’s demand and appears to be keeping up this time.

Meanwhile, it’s not just about Quest 2. There’s momentum elsewhere in the VR market as PSVR remains the market share leader for the time being, and could see updates soon given the advent of PS5. And other hardware remains compelling such as Valve Index and HP Reverb G2.

Altogether, ARtillery Intelligence estimates that Quest (all variants) sold 770,000 units in 2021, growing to 1.42 million this year. The VR market could collectively sell 6.1 million units for tier 1 & 2 headsets (sans mobile VR), which correlates to a cumulative installed base of 16.4 million units.

Pandemic-Proof?

Everything mentioned so far is consumer-oriented… What about enterprise AR? It won’t reach its tipping point in 2021 but that could come in 2022. Meanwhile, the sector will make progress in 2021 — less with the tech than with organizational acceptance, which is what it needs most.

Enterprise AR meanwhile benefits from Covid and post-Covid dynamics, such as guided support for distanced work. Speaking of which, the ongoing global pandemic will impact all of the above spatial sub-sectors unevenly. Put another way, some are more pandemic-proof than others.

Mobile AR for example will be less affected because it’s software, and it’s aligned with Covid-era demand signals like entertainment, communications and commerce. VR has suffered from supply-chain issues, but it also has Covid-alignment in gaming and remote collaboration.

There will continue to be lots of uncertainty in all these areas as the world transitions from a pandemic. But one thing we can expect is continued forward movement as spatial computing enters adolescence. See the full episode below, and access the full report here.